Topics

-

Fifty-five women engineering students completed an AI bootcamp focused on rural Karnataka. Participants developed AI-based solutions after visiting villages and conducting field interviews. The She Innovates bootcamp partnered with several organizations to achieve its goals. This initiative aims to boost women's participation in AI and entrepreneurship. It encourages AI applications for rural development and community-focused sectors. View the full article

-

Besi's quarterly orders more than doubled, fueled by AI and hybrid bonding technology. The company saw increased customer adoption of its advanced chip packaging solutions. Demand for AI applications continues to drive growth in data centers. Besi anticipates revenue growth between ten and fifteen percent. This strong performance aligns with other semiconductor sector reports. View the full article

Leaderboard

-

Mohamed Asif Abdul Hameed

Fraternity Members2Points78Posts

Popular Content

Showing content with the highest reputation on 08/11/2020 in all areas

-

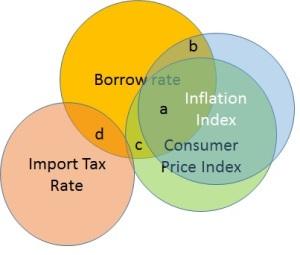

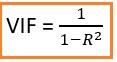

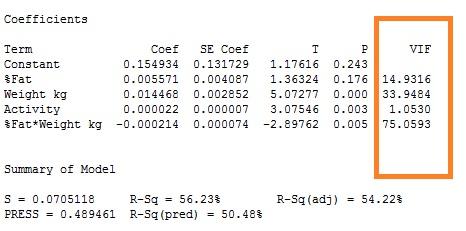

Multicollinearity is a statistical phenomenon. It happens when several independent variables are highly correlated, However not perfectly correlated and In this situation we get regression results to be unreliable. In the above example, we could see how and to what extend does Consumer Price Index and Inflation Index can predict the rates. There is a considerable overlap between Consumer Price Index and Borrow Rate and Substantial overlap between Inflation Index and Borrow rate. Now, because there is a significant overlap between Consumer Price Index and Inflation Index themselves. It would be possible to predict with the unique non-overlapping contribution. Unique non-overlapping contribution of Consumer Price Index is Area c and Unique non-overlapping contribution of Inflation Index is Area b and Area a will be lost to standard error. Why Multicollinearity is considered as a problem? We would not be able to discriminate the individual effects of the independent variables on the dependent variable Further Correlated independent variables make it hard to make inference about individual regression coefficients and their effects on dependent variable. As a result, it is difficult to disprove Null Hypothesis, wherein actually the same should be rejected. Multicollinearity might not affect the accuracy of the model by a lot. But we might lose reliability in determining the effects of individual features of the model and that can be a problem when it comes to interpretability. How do we detect Multicollinearity? By using scatter plot or by using correlation matrix it would be possible to detect multicollinearity with regards to bivariate relationship between variables It can be detected based on Variance Inflation Factor or as popularly referred as VIF. VIF score of independent variable represents how well the variable is explained by other independent variables. When R2 value is close to 1, higher the value of VIF and higher the multicollinearity with the independent variable. VIF = 1 implies No correlation between independent variables and other variables VIF > 5, indicates high multicollinearity Diagnosis and Fix: Dropping one of the correlated features can bring down multicollinearity significantly Priority of dropping variable is based on the high VIF value Combining correlated variables into one and drop the others Points to remember before fixing: Removing multicollinearity will be a good option when more preference is given to individual features relatively to the group features that impact the focus variable Efficient corrective action to remove multicollinearity requires selectivity and selectivity in turn requires specifics about the nature of the problem.

2 points

2 points

This leaderboard is set to Kolkata/GMT+05:30