Dinesh_Tiwari_WBim

Members

-

Joined

-

Last visited

Everything posted by Dinesh_Tiwari_WBim

-

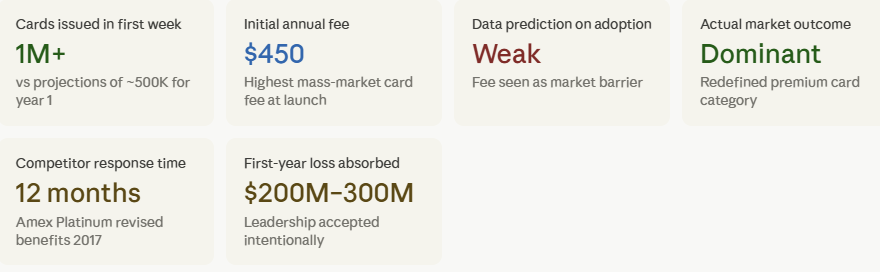

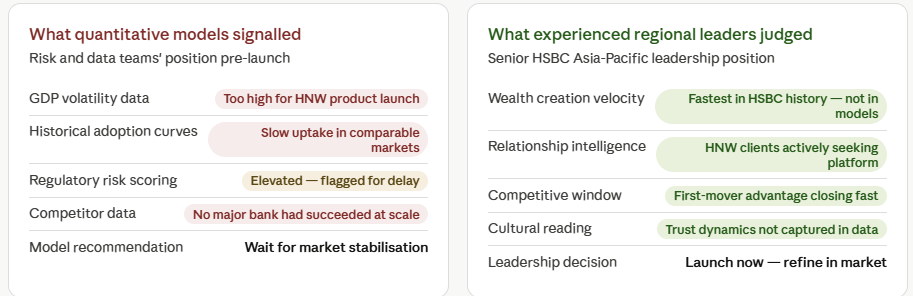

Dinesh_Tiwari_WBim replied to Vishwadeep Khatri's topic in We ask and you answer! The best answer wins!This is interesting case and I will support View B - Trust Experienced Leadership Judgment. Data Sees the Past. Leaders See the Moment. Every transformational product launch in banking history looked questionable in the data before it succeeded. AI reads patterns from what has already happened. Leaders read the market as it is becoming. When those two perspectives conflict on a time-critical launch decision, the human with years of market intuition, relationship intelligence, and competitive instinct deserves the deciding vote not the algorithm. Reframing the dilemma: The AI system in this scenario is doing exactly what it is designed to do: analyzing historical usage patterns, comparable market data, and early signals to generate a probability-weighted prediction. That prediction deserves serious consideration. It should be stress-tested, debated, and used to sharpen the launch strategy. What it should not do is override the judgment of experienced leaders who are reading signals the AI cannot access — signals about competitive urgency, relationship timing, organizational momentum, and market psychology that do not exist in any training dataset. The most dangerous version of AI adoption is not one where AI gives wrong answers. It is one where organizations build governance structures that allow statistically conservative AI predictions to veto bold, well-reasoned human conviction at exactly the moments when boldness is what the competitive situation demands. Example 1- from Banking world: JPMorgan Chase and the launch of Chase Sapphire Reserve when every data signal said wait, and leadership said launch: What the data said vs what leadership saw — and what actually happened **Year 1 loss was strategically acceptable as lifetime value of HNW millennial relationship justified the acquisition cost. Example 2 - HSBC and the 2013 emerging markets wealth expansion Three things AI cannot do in a launch decision 1- AI cannot read the room. The competitive intelligence that informed JPMorgan leadership's decision their understanding of Amex's internal priorities, their reading of millennial consumer psychology, their sense of the cultural moment in which a premium travel card would become a status signal came from decades of relationship-building, market observation, and pattern recognition across hundreds of competitive situations. This is not data. It is wisdom. No training dataset captures it, and no model can replicate it. 2- AI cannot assess its own blind spots. When the data model predicted weak adoption, it had no mechanism to flag that its training data contained no examples of the market segment being created because that segment did not yet exist. It treated the absence of confirming evidence as evidence of absence. Experienced leaders knew to ask the question the model could not: "Is this a market where our data is relevant, or are we creating something genuinely new?" That meta-judgment about when to trust the model and when to override it is itself a leadership capability that cannot be outsourced to AI. 3- AI cannot generate organizational conviction. The energy with which JPMorgan's teams executed the Sapphire Reserve launch the partnership negotiations, the marketing campaign, the customer service preparation, the card stock manufacturing commitment was powered by senior leadership's visible, committed, conviction-driven endorsement of the decision. A data-hedged, committee-approved, AI-validated launch produces a different energy entirely. Leadership conviction is a launch variable with direct bearing on execution quality and market impact. It is not replaceable by statistical confidence intervals. The Bottom line: The AI system in this scenario is not wrong to raise its concerns. Weak adoption signals, retention risk, and first-year loss projections are real inputs that deserve serious consideration. They should be debated, stress-tested, and used to sharpen the launch plan. What they should not do is govern the decision. JPMorgan's leadership team looked at the same risk signals in 2016, weighed them against their reading of the competitive environment, the customer segment, and the strategic moment — and launched anyway. Within seven days, the data model's central prediction was invalidated. Within two years, the product had redefined a category. Within seven years, it had become a case study in exactly the kind of bold, well-reasoned, conviction-driven leadership judgment that no AI system can replicate. Markets are shaped by timing, vision, and human intuition. Breakthrough decisions look risky in the data before they succeed — because the data cannot see what leaders can. When experienced leaders and AI predictions disagree on a time-critical launch decision, the right governance structure is one where AI informs and humans decide. Trust the judgment. Back the conviction. Launch with excellence. That is what leadership is for.

-

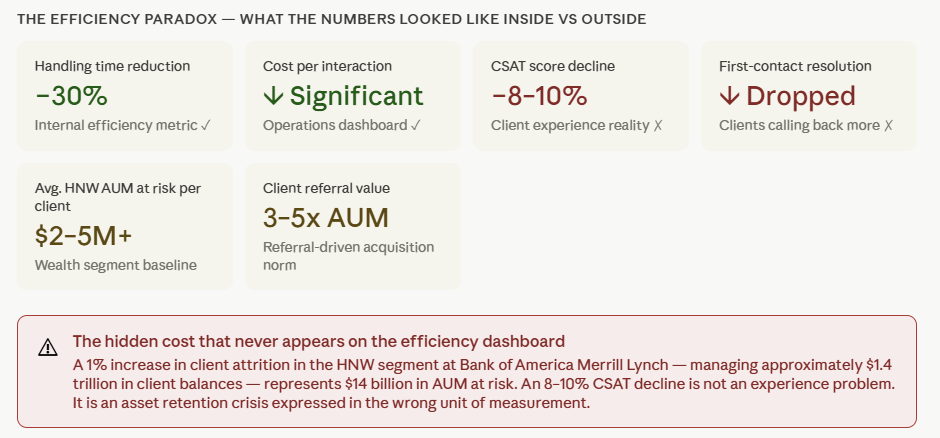

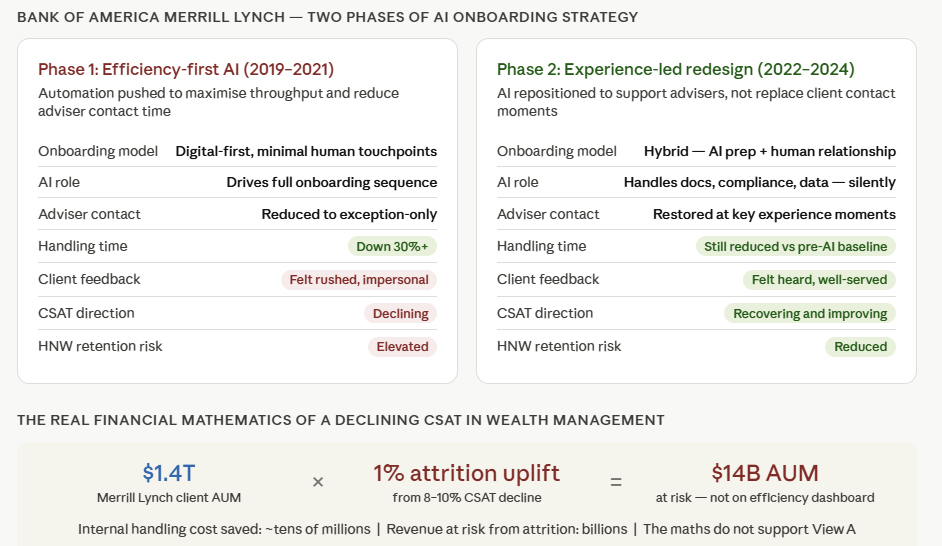

Dinesh_Tiwari_WBim replied to Vishwadeep Khatri's topic in We ask and you answer! The best answer wins!I will support View B - Reject or Rethink This Change. Efficiency That Destroys Trust Is Not Progress — It Is a Slow Catastrophe. If I talk about the banking industry, a 30% reduction in handling time means nothing if the client on the other end of that interaction is deciding to move their assets elsewhere. In wealth management, customer experience is not a soft metric sitting alongside the real numbers — it is the real number. It determines whether clients stay, consolidate, and refer. Everything else is overhead. View A presents efficiency and customer experience as a trade-off where efficiency comes first and experience can be fixed later. In most industries, this sequencing is debatable. In wealth management client onboarding, it is categorically wrong — and the evidence from Bank of America's own journey makes this case with unusual clarity. Example: Bank of America Merrill Lynch — when efficiency-first AI met wealth management realityBank of America's wealth management division operating under the Merrill Lynch and Bank of America Private Bank brands — provides one of the most instructive and well-documented cases of what happens when internal efficiency optimisation is prioritised over client experience in a high-value onboarding context. Sharing below five reasons to Reject and Rethink: Revenue protection. The AUM mathematics are unambiguous. Handling cost savings in wealth management onboarding are measured in the tens of millions. AUM at risk from a trust-driven attrition increase is measured in the billions. No board that understands this arithmetic approves the efficiency-first model. Brand and market position. Merrill Lynch's proposition — "the Thundering Herd," personal expertise, relationship-led wealth management — is not a marketing tagline. It is the reason clients choose this institution over a robo-adviser or a digital-only platform. An onboarding model that makes clients feel like they have chosen the wrong type of institution does not just lose that client. It validates the competitor's value proposition. Referral economics. The highest-returning client acquisition channel in wealth management is peer referral from existing satisfied clients. A single dissatisfied HNW client who stops referring costs the institution not one relationship — it costs the entire referral network that client would have activated over the next five to ten years. This cost never appears on the efficiency dashboard that approved the AI deployment. First-contact resolution economics. The drop in FCR creates a perverse efficiency outcome: clients who were rushed through interactions call back more frequently, each callback requiring more time and more resource than the extended original interaction would have. The headline 30% handling time reduction is partially clawed back by increased repeat contact volume. The efficiency case becomes self-defeating on its own terms. Regulatory and conduct risk. In the UK, FCA Consumer Duty regulations introduced in 2023 place a legal obligation on financial institutions to demonstrate that they are delivering good outcomes for clients — not just efficient processes. An AI-driven onboarding model that demonstrably reduces client understanding, produces lower FCR, and generates declining satisfaction scores is not a neutral operational choice. It is a potential conduct risk event. The regulator's question — "did your client genuinely understand what they were signing up for?" — does not get a satisfactory answer from a process optimised to minimise the time spent answering it. The current AI deployment as described must be rejected and rethought - Rethink the design. Reposition the AI. Rebuild the experience. That is the only version of this change worth accepting.

-

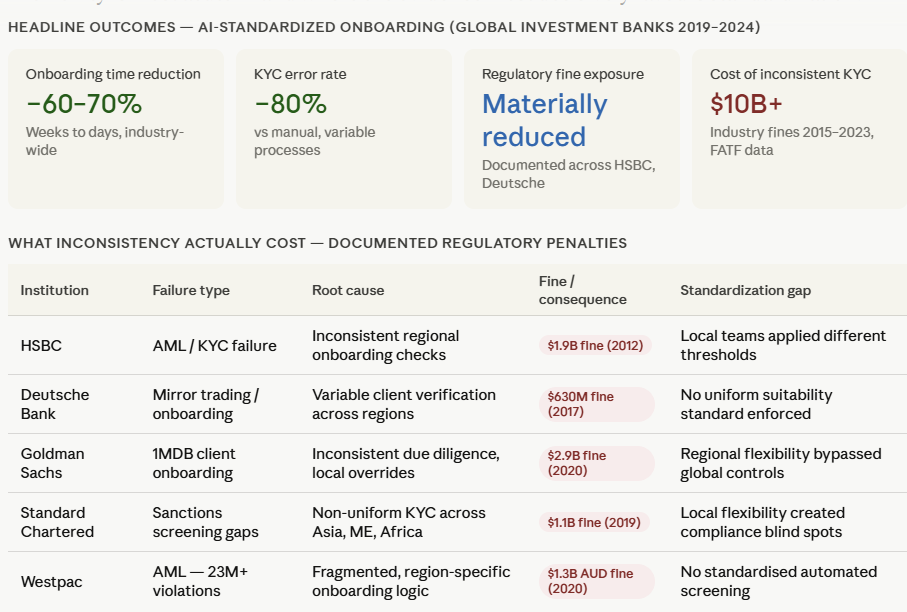

Dinesh_Tiwari_WBim replied to Vishwadeep Khatri's topic in We ask and you answer! The best answer wins!I will go with View A- Embrace standardization. Consistency improves quality, reduces errors, and makes scaling easier. Standardized AI-driven decisions are more reliable than variable human judgment. When a global investment bank onboards a high-net-worth client onto a trading platform, the cost of inconsistency is not only different customer experience, but also a regulatory breach, a compliance failure, or a reputational event. In that environment, standardization is not a constraint. It is the foundation on which trust is built. If I talk about View B, it frames standardization as the enemy of good judgment. But this framing misunderstands what standardization actually does in a complex, regulated, multi-region operation. Standardization does not eliminate judgment, it elevates it. It removes the low-value variability that comes from inconsistent training, individual habit, and regional interpretation of rules, and it creates the headroom for genuine human judgment to operate where it truly matters. Sharing an example of AI-driven client onboarding in wealth management trading platformsThe most compelling evidence for View A comes directly from the client onboarding operations of global investment banks, specifically, the Know Your Customer (KYC), Anti-Money Laundering (AML), suitability assessment, and account activation workflows that govern how high-net-worth and ultra-high-net-worth clients are brought onto trading platforms. Sharing few reasons how standardization wins and creates an impact: Impact: Regulatory and legal. In the five cases documented above — HSBC, Deutsche, Goldman, Standard Chartered, Westpac — the combined regulatory penalty exceeded $7.8 billion. Every single case was rooted in regional inconsistency of onboarding and client verification standards. AI standardization is not just an efficiency measures, it is a legal liability reduction strategy of the first order. Impact: Client experience. The wealthiest clients in the world operate across multiple jurisdictions. They choose banks that deliver the same quality of rigor and speed regardless of where they are being served. When UBS standardized its onboarding, its NPS scores improved — because clients experienced consistency as quality, not as inflexibility. Impact: Operational scalability. A bank expanding wealth management into a new market must currently rebuild institutional knowledge, train local compliance teams, and hope that standards transfer correctly. With AI standardization, the engine carries the standard automatically. Expansion becomes a deployment exercise, not a capability-rebuilding exercise. This is a fundamental shift in how global financial institutions can grow. Impact: Talent and training. When the standard is embedded in AI, new relationship managers learn from a reliable, consistent framework from day one. JPMorgan saw a 40% reduction in onboarding training time. This is not because people learn less, it is because they learn the right things consistently, rather than absorbing the idiosyncratic habits of whoever trained them. Impact: Auditability and governance. In a regulatory environment defined by MiFID II, FATF standards, GDPR, and local central bank requirements, the ability to reconstruct every onboarding decision from a complete, structured audit trail is not optional it is the minimum standard. Manual, flexible processes cannot provide this reliably. AI-standardized processes produce it automatically. The global investment banks that have committed to AI-standardized onboarding are not sacrificing quality for efficiency. They are doing something more important using human intelligence: they are making their best practice available to every client, in every region, on every onboarding, every single time. That is what a premium wealth management institution owes its clients and its regulators. Embrace standardization!

-

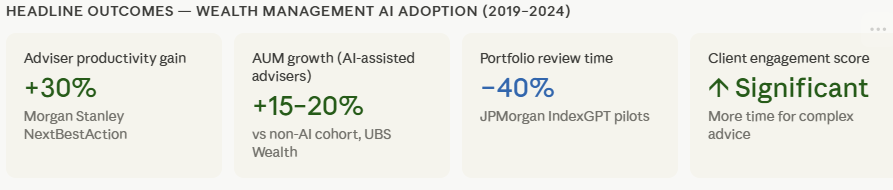

Dinesh_Tiwari_WBim replied to Vishwadeep Khatri's topic in We ask and you answer! The best answer wins!I will go in favor of View A — Continue Relying on AI Headline: Every major technology shift in history has changed what humans do, not eliminated the need for humans. AI in operations is no different. The question is not whether to rely on it, but how to evolve alongside it. Reframing the dilemmaThe concern embedded in View B is legitimate on its surface: if people stop practicing a skill, they get worse at it. That is simply true. But the conclusion drawn — that we should therefore limit AI reliance — makes the same logical error as arguing that calculators should be banned because students stop practicing long division. In operations environments, the skills most threatened by AI manual data aggregation, rule-based prioritization, high-volume routine decision-making are not the skills that define organizational resilience. What defines resilience is judgment, client understanding, ethical reasoning, and the ability to navigate genuinely novel situations. AI does not erode those. Example from Real world: AI adoption in Wealth Management at global investment banksThis is not a theoretical argument. The wealth management divisions of JPMorgan, Morgan Stanley, and UBS have provided some of the most documented and measurable evidence of what AI adoption actually does to human capability and it is not what View B predicts. Impact of continuing AI adoption in wealth management operations: Financial impact — measurable AUM and revenue growth Morgan Stanley advisers supported by AI generated meaningfully higher AUM growth. UBS documented 15–20% higher AUM with AI-assisted advisers vs the non-AI cohort. These are not projected gains — they are audited outcomes across thousands of client relationships. Operational impact — 360,000 hours of human capacity released JPMorgan's COiN system eliminated over 360,000 hours of manual contract review annually. That capacity did not disappear — it was redeployed into client strategy, risk oversight, and relationship management. The organization grew more capable, not less. Client impact — higher-quality advice at scale When advisers are no longer consumed by data aggregation and routine rebalancing, they spend more time understanding individual client goals. Client satisfaction scores and retention rates improved across all three firms post-AI implementation. Talent impact — advisers become more valuable, not redundant Contrary to View B's concern, advisers at AI-enabled firms did not atrophy. They upskilled. The role evolved from data processor to trusted adviser. Junior staff exposure to complex client scenarios increased because AI removed the queue of routine work that previously dominated their time. Risk impact — AI handles high-volume compliance, humans handle judgment Regulatory compliance monitoring — KYC checks, transaction surveillance, suitability assessments was automated at scale, reducing human error in repetitive review tasks. Human oversight was preserved for cases requiring contextual judgment, precisely where it matters most. Strategic impact — competitive differentiation and market positioning Firms that limited AI adoption during this period fell behind on response times, personalization capability, and cost efficiency. The wealth management clients of AI-enabled banks received more proactive, better-timed, and more personalized service — and they noticed. The bottom lineThe historical analogy is direct: when Bloomberg terminals entered wealth management in the 1980s, experienced managers raised exactly the same concern as View B that traders and analysts would lose their ability to reason without real-time data feeds. What actually happened is that the profession deepened. Those who adapted became better analysts. Those who refused the technology became irrelevant. AI in operations is that moment again. The organizations that continue to rely on AI thoughtfully, with governance, with investment in human skill evolution will be the ones that define what excellent wealth management looks like in the decade ahead. The ones that hold back, in the name of preserving capabilities that AI has already surpassed, will find themselves defending a standard their clients no longer value. Continue the adoption. Invest in the evolution. That is the only position consistent with the evidence.

-

Dinesh_Tiwari_WBim replied to Vishwadeep Khatri's topic in We ask and you answer! The best answer wins!I am in support of view B- Do not adopt the AI system in its current form. When we talk about "average improvement," we are talking about what happens to the majority of operations under normal conditions. But leaders are not ultimately judged on averages. They are judged on how their systems behave when things go wrong. A 15% improvement in on-time performance sounds like a strong headline — until you understand that the same system has also introduced a new category of failure that did not exist before: a tightly wound, buffer-free schedule that, when disrupted, unravels everything downstream simultaneously. The question we must honestly ask is: are we willing to trade a predictable, moderate-variance system for one that is brilliant most of the time but structurally incapable of absorbing shock? The real-world banking case: Citigroup's 2020 operational failureTo make this concrete, let me draw from one of the most documented and costly operational failures in recent banking history — one that has direct parallels to the AI scheduling dilemma we face. In August 2020, Citigroup accidentally transferred approximately $900 million to creditors of Revlon Inc. — a loan repayment they did not intend to make. The root cause was not a rogue employee or a cyberattack. It was a combination of outdated, highly optimized legacy software (Flexcube) and a tightly engineered workflow with no meaningful error-checking buffer. The system was optimized for speed and efficiency in routine transactions. It had virtually no tolerance for edge-case human input errors. The operational failure led to a $400 million regulatory fine from the OCC and Federal Reserve in 2021, years of costly litigation, permanent reputational damage with institutional clients, and a forced commitment to spend over $1 billion on remediation of risk and control infrastructure. This is a real example of an optimized system — one that performed excellently in the vast majority of cases — producing a catastrophic tail-event outcome because robustness had been sacrificed for efficiency. What this means to an organization?There is a common trap in boardroom AI discussions: we celebrate the average case and footnote the tail. The Citigroup example is a reminder that the tail is where reputations are destroyed, regulators appear, and billions are spent. Here is how wrong adoption of AI tool will impact the organization: Impact: Financial The 15% average efficiency gain applies to 97–98% of operations. The 2–3% failure cases carry costs — compensation, emergency ops, rebooking, crew overtime — that are not linear. A single cascading event at a hub airport can cost more than weeks of efficiency savings. Citigroup's $400M fine came from one transaction. The financial math of tail events does not favor optimistic averaging. Impact: Reputational Customers do not experience your average. They experience their flight. A stranded passenger telling their story on social media is more powerful than a press release about improved on-time statistics. Brands in aviation and banking are built on reliability — a word that is fundamentally about tail behavior, not average behavior. Impact: Regulatory Regulators in aviation (DGCA, FAA, EASA) and banking (RBI, OCC, Fed) do not accept "it works most of the time" as a compliance position. A documented structural gap — a system that knowingly removes buffers in 2–3% of cases — is a regulatory liability waiting to be activated. Impact: Operational morale Frontline teams who repeatedly scramble to manage AI-triggered crises will lose trust in the system. Shadow procedures emerge. The AI's recommendations get quietly ignored. The investment fails not because the technology is wrong, but because adoption was forced before robustness was proven. My recommendation:Do not reject this AI Toll. Require it to be rebuilt correctly before deployment. Specifically, insist on three non-negotiable design conditions before any sign-off: First, a minimum buffer floor — the system must never optimize away below a configurable safety threshold, regardless of what the algorithm recommends. The efficiency gain is acceptable only above that floor. Second, stress-test reporting — before live deployment, the system must run 12 months of historical disruption scenarios and demonstrate its failure rate and recovery profile. We should see its tail behavior before we own it. Third, a supervised pilot phase — the AI runs in advisory mode alongside human schedulers for 90 days. Efficiency gains are measured. Tail events are documented. Only then does full autonomy expand. This is not a rejection of innovation. It is the standard of care that distinguishes those who adopt AI wisely from those who adopt it quickly.