All Activity

- Past hour

-

Vishwadeep Khatri replied to Vishwadeep Khatri's topic in We ask and you answer! The best answer wins!1. rajan.arora2000 Position: View B (Human must own the off-switch — AI cannot price the discovery value of improvement) Specific Example: A six-case matched portfolio including Intel FDIV bug, Kodak, Boeing 787, Netflix, IBM PC, and Toyota's andon cord; cites Dixit & Pindyck (1994) on real-options theory and James G. March (1991) on exploration vs. exploitation. Reasoning Quality: Highly sophisticated — introduces two original coined structures (the Truncated Objective and the Optimization Ratchet), applies real-options theory to argue that naive NPV misses discovery value and option value, and adds an AI-specific feedback loop showing how the model retrains itself toward further stops. 2. Raja M Position: View A (Accept the AI's recommendation) Specific Example: Amazon Fire Phone — discontinued and capital redirected to AWS, Alexa, and logistics automation, yielding transformational returns; also provides a structured seven-factor decision framework. Reasoning Quality: Good — frames the argument clearly around resource allocation and opportunity cost; the Fire Phone example is a product discontinuation case rather than a direct manufacturing yield analogy, but the strategic logic is sound and well-structured. 3. Suhail_J Position: View A (Accept the AI's recommendation) Specific Example: Toyota's internal analysis concluding that a paint-line improvement was technically possible but economically unjustifiable, redirecting resources to new model development and battery technology. Reasoning Quality: Good — uses the precise technical framing of the system being noise-limited rather than design-limited, and correctly characterises the asymptotic zone; however, the Toyota paint-line example is asserted without a verifiable source or documented outcome. 4. Abhishek Adhikary Position: View A (Accept the AI's recommendation) Specific Example: Toyota Lean principle that Kaizen selects improvements by highest impact, not by endless pursuit; Intel's shift from clock-speed marginal gains to multi-core architectures, energy efficiency, and AI accelerators. Reasoning Quality: Good — makes a strong conceptual distinction between "can we improve" versus "is this the best place to improve," and correctly invokes Toyota's Lean philosophy eliminating waste where it creates greatest value. 5. Naijur Rahman Position: View A (Accept the AI's recommendation) Specific Example: Toyota Prius MPG improvement curve (documented generational gains declining from 5 mpg to 2 mpg) with Toyota's documented $13.5B redirect to solid-state battery R&D; Amazon AWS ($107B revenue, 37% operating margin) vs. North American retail (4.5% margin); Apple MacBook Retina display decision (2012); sigma-level cost table showing 4.4σ current position; NPV calculation with 10–12% hurdle rate. Reasoning Quality: Exceptional — the most quantitatively rigorous answer in the thread, grounding the diminishing-returns argument in documented sigma-level data, a concrete NPV framework, and three named real-world examples with specific financial figures and cited sources. 6. Ajay Wadhwa Position: View A (Accept the AI's recommendation) Specific Example: Toyota Production System and the distinction between improving and "just staying busy"; invokes TPS over-processing waste principle. Reasoning Quality: Competent — makes the opportunity cost argument clearly and applies the TPS waste framework appropriately; the response is concise and the reasoning is correct, though it does not cite a specific named case study with documented outcomes beyond the TPS principle itself. 7. Prateek Harsh Position: View A (Accept the AI's recommendation) Specific Example: Intel's retirement of the Tick-Tock cadence (2015) when marginal node shrinks became economically unjustifiable, redirecting to the Process-Architecture-Optimization model; automotive industry redirecting from marginal combustion-engine MPG gains to hybrid/EV powertrains and SUVs, citing National Research Council data on cylinder deactivation cost. Reasoning Quality: Good — two well-chosen examples, both with documented outcomes; the Intel Tick-Tock case is a direct parallel to the dilemma. 8. Ankita Bhardwaj Position: View A (Accept the AI's recommendation) Specific Example: Fujifilm vs. Kodak — Fujifilm redirected $9B capital to medical diagnostics and LCD coatings while Kodak over-indexed on film improvement, leading to its 2012 bankruptcy; Motorola Iridium — $5B invested in a technically perfect satellite network that went bankrupt in 1999 with fewer than 20,000 subscribers; also introduces an original Strategic Feasibility Index (SFI = 0.0213) framework. Reasoning Quality: High quality — introduces the Kaizen vs. Kaikaku distinction, two strong matched examples with documented financial figures, and a quantitative SFI framework. 9. Bedibrat Kutum Position: View A (Accept the AI's recommendation) Specific Example: Toyota's Kaizen investment-shift at plants where diminishing returns appeared, redirecting to new models, supply base, and regional capacity; Intel Tick-Tock adaptation when the physics of manufacturing made the pace financially unsustainable. Reasoning Quality: Good — makes a meaningful distinction between the culture of continuous improvement and an imperative to spend regardless of outcome; examples are sound, though presented at a general level without specific plant-level or financial citations. 10. Vinit Dubey Position: View B (Continue pursuing every worthwhile improvement — AI should inform but not decide) Specific Example: Toyota (Kaizen with sub-second cycle time gains), British Cycling (1% marginal gains philosophy), Apple (consistent incremental improvements), Amazon (continuous logistics refinement); also provides a strategic lens comparison table. Reasoning Quality: Good — makes a legitimate case that ROI-only evaluation misses strategic value, long-term compounding, competitor dynamics, and regulatory risk; the examples function more as illustrations of continuous improvement culture than specific cases of pursuing improvements beyond performance ceilings. 11. anthony rebello Position: View A (Accept the AI's recommendation) Specific Example: Toyota over-processing waste (Muda) — Kaizen explicitly classifies over-quality as waste; Intel/TSMC semiconductor yield — fabricators target economically optimal yield, not maximum, because the cost of removing final defects rises exponentially; Netflix — redirected from optimising DVD-by-mail excellence to streaming and original content. Reasoning Quality: Good — correctly identifies Toyota's over-processing Muda principle as directly applicable, uses Intel/TSMC as a direct manufacturing analogy to the dilemma, and the Netflix example illustrates strategic frontier-shifting. 12. Saran raj Venkatesan Position: View A (Accept the AI's recommendation) Specific Example: Five matched-pair cases across sectors — Intel vs. AMD semiconductor strategy (2012–2019, documented in annual reports); Japanese DRAM manufacturers vs. Samsung/Hynix (1990s–2000s, Langlois & Steinmueller 1999); Toyota's Seven Wastes over-processing principle (Ohno 1978); Mercedes-AMG F1 vs. Red Bull (2022); Kodak film excellence vs. digital photography; also presents a formal NPV sign-condition model and the original INVEST Framework (6 gates). Reasoning Quality: Exceptional — the most empirically comprehensive answer in the thread, with five named cases across four sectors, formal mathematical modelling, and an original deployable framework. 13. Dinesh Selvarajan Position: View B (Continue pursuing every worthwhile improvement) Specific Example: Nokia and Kodak — cited as companies that stopped pushing improvement boundaries and lost competitiveness; also references the Kano model and DMAIC/DMADV. Reasoning Quality: Competent — makes the competitor-monitoring argument and applies the Kano model appropriately to explain how quality thresholds shift over time; however, Nokia and Kodak are cited only by name as cautionary tales without specific detail about the marginal improvement decisions that led to their decline. 14. Adeniran Ilesanmi Position: View A (Accept the AI's recommendation) Specific Example: Juran/Feigenbaum cost-of-quality curve — at 99.8%, the organisation is likely past the optimum total cost point; NPV test at 10–12% industrial hurdle rate requiring $3.2–3.5M/year to break even; Intel semiconductor fabs — reject uptime improvements requiring multi-million equipment redesign and redirect to next-generation lithography; Delta Airlines — stopped pushing OTP from 95% to 96% and invested in customer experience and fleet modernisation instead. Reasoning Quality: High quality — applies established quality economics theory with a specific quantitative NPV test and two named organisational examples with specific cost and decision details. 15. kartik voleti Position: View A (Accept the AI's recommendation) Specific Example: Toyota — as vehicle quality reached world-class levels, shifted investment toward hybrid technology and electrification (Prius as world's first mass-market hybrid, multi-year market leadership); Amazon — redirected internal infrastructure investment to AWS commercial platform, now generating the majority of Amazon's profit. Reasoning Quality: Good — both examples are well-chosen and logically connected to the argument; the Toyota/Prius case is specific and documented, and the response correctly identifies that Kaizen requires selecting improvements by highest customer and business value. 16. Sunil Emandi Position: View A (Accept the AI's recommendation) Specific Example: Intel (1985–87) — exited memory chips entirely and redirected all capacity to microprocessors, with Andy Grove's attributed quotation: "Most companies don't die because they are wrong; most die because they don't commit themselves"; four-case "Stop Doing List" portfolio; also directly rebuts the View B counterargument that a competitor might close the 0.1% yield gap. Reasoning Quality: High quality — uses a powerful and specific historical case with an attributed quotation, directly addresses and rebuts the main View B counterarguments, and makes the precise sequencing point that distinguishes strategic reallocation from complacency. 🏆 Winner: Naijur Rahman Naijur Rahman's answer wins across all three comparative criteria. On clarity of position, it is unambiguous and frames the question as a manufacturing-science problem before addressing it as a financial one. On quality and completeness of reasoning, no other answer in the thread constructs the sigma-level cost table with documented DPMO data, applies a specific industrial hurdle-rate NPV break-even calculation, or explicitly names and explains the psychological biases — escalation of commitment, status quo bias, sunk cost — that cause the executives' resistance, making it the only answer that accounts for why the problem exists and not just what the answer is. On relevance and specificity of examples, it presents three named cases with specific financial data: the Toyota Prius generational MPG curve (documented across four vehicle generations with the $13.5B battery R&D redirect), Amazon AWS vs. North American retail margin comparison (Q4 2024 figures cited), and Apple's MacBook Retina display decision (227 ppi, 2012). Compared to other approved answers — which each offer one or two strong examples and sound reasoning — Naijur Rahman's answer is distinctively more complete in its analytical architecture: manufacturing science framework first, financial framework second, behavioural economics third, making it the clearest and most deployable answer in the thread.

- Today

-

Ankita_Bhardwaj_gN3V changed their profile photo

-

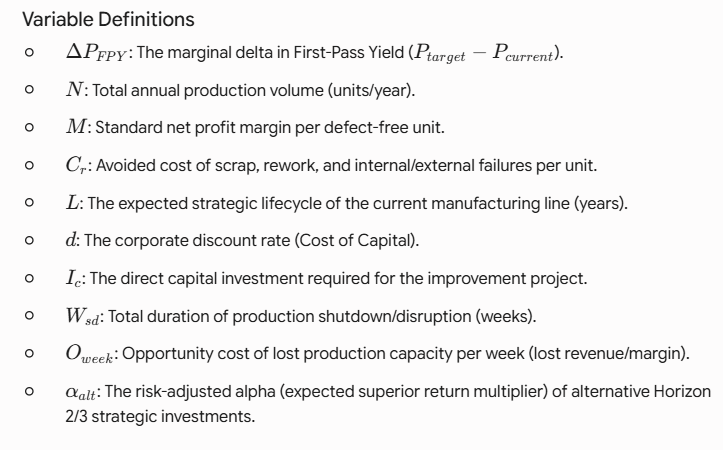

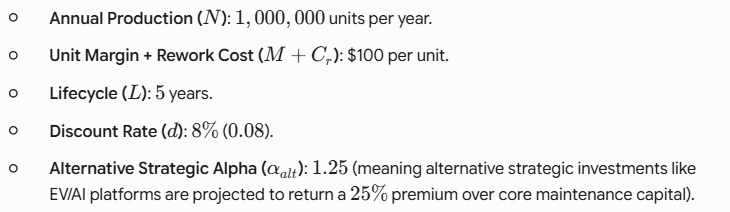

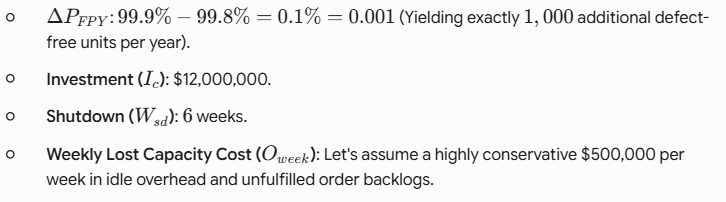

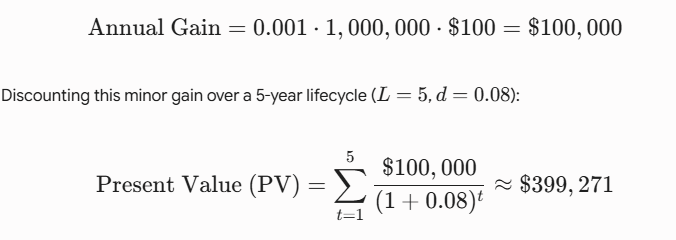

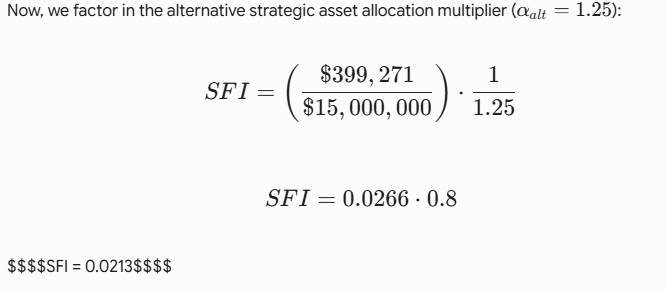

Position: View A — Accept the AI’s recommendation. The executives resisting it aren’t being more ambitious. They’re being less strategic.The AI Didn’t Blink. The Executives Did.Peter Drucker wrote in The Effective Executive: “There is nothing so useless as doing efficiently that which should not be done at all.” This is precisely the diagnostic the AI applied — and the executives in the room missed it entirely. The disagreement in the boardroom is being framed as “should we keep improving?” That is the wrong question. The AI isn’t arguing against improvement. It is arguing against this improvement, at this time, at this cost, for this return. A company that has achieved 99.4% on-time delivery, 99.8% first-pass yield, and an 18% cost reduction in two years is not a struggling operation in need of a push. It is a high-performing operation in need of a strategic question: where does the next $12M create the most value? The executives who disagree are confusing a philosophy (continuous improvement is always virtuous) with a decision (this specific investment is worth making now). Those are not the same thing, and collapsing that distinction is how organizations burn capital chasing diminishing fractions. What the Drucker Test Reveals That the Boardroom MissedThe core test for any improvement investment is not: Can we do it? — the AI agrees you can. The test is: Does the expected return, net of disruption, exceed the cost of capital and the opportunity cost of the best alternative use of that $12M? Laid out plainly: Proceed only if: NPV of improvement > (Capital cost + 6-week disruption loss) + Opportunity cost of next-best use In this case, the AI has already run this logic. “Marginal financial returns over five years” is not a passing grade on a $12M investment with a 6-week production freeze. The return is below the hurdle. The disruption is above the tolerance. And — critically — no one in the room has named what else $12M could accomplish for a company already operating at elite efficiency levels. That silence is telling. When the alternative isn’t named, the status quo gets falsely elevated. Bex is directionally right but builds the argument on a single example (Toyota) without pricing in the opportunity cost, which is the central variable the AI is calculating. When Doing It Better Is the Worst Thing You Can DoJim Collins warned in Good to Great: “Equally important, create a ‘stop doing list’ and systematically unplug anything extraneous.” His research showed that the companies which made the leap from good to great were not the ones who did more — they were the ones who ruthlessly identified what to stop doing and freed up resources to concentrate on what mattered. The executive instinct to pursue 99.9% is not wrong in principle. It is wrong in sequencing. At 99.8% yield, the marginal improvement curve is nearly vertical — you’re spending exponentially more for linearly less return. The company has already harvested the bulk of available efficiency. Every dollar spent on the next 0.1% is a dollar not spent on new markets, product innovation, capacity expansion, or talent investment — all of which likely carry higher returns. The “stop doing list” is not a white flag. It is a reallocation instrument. And the AI just handed leadership one. Four Times the ‘Stop Doing List’ Outran the ‘To-Do List’Case The Marginal Improvement Being Chased What Was Done Instead What Happened Intel (1985–87) Intel had been a memory chip company for 17 years. With Japanese competitors slashing prices and taking share, Intel faced a choice: keep investing to marginally improve memory chips, or redirect. Gordon Moore and Andy Grove famously asked each other: “If a new CEO walked in tomorrow, what would they do?” The answer was unambiguous: exit memory. Redirected all manufacturing capacity and R&D to microprocessors — a smaller, less proven business at the time. Intel became the world’s most dominant chip company. Grove later wrote in Only the Paranoid Survive: “Most companies don’t die because they are wrong; most die because they don’t commit themselves. They fritter away their valuable resources.” Intel committed. Microsoft under Satya Nadella (2014) In 2014, Microsoft was still investing heavily in incremental Windows improvements and Windows Phone — a mobile effort that had under 3% market share despite billions spent. The marginal gain on each Windows release was declining. Enterprise clients were already moving to cloud. Nadella accepted that the Windows-centric model was a diminishing return. He redirected capital aggressively to Azure cloud infrastructure, even when AWS had a seven-year head start and analysts were skeptical. Microsoft’s market cap grew from approximately $300 billion in 2014 to over $3 trillion by 2024. Azure now supports 95% of Fortune 500 companies. The decision to stop chasing Windows marginal gains was the pivot that made it the most valuable technology company on Earth. Procter & Gamble (2014) P&G had 165 brands in its portfolio. Roughly 100 of them were contributing marginally — average 3% annual sales decline and profits 16% below company average. The organization was investing time, shelf space, and marketing dollars in these underperformers in the name of “continuing to compete.” CEO A.G. Lafley publicly pruned approximately 100 brands, focusing resources on the 65 that generated 95% of the company’s profits. He called it creating “a much simpler, much less complex company of leading brands.” P&G’s margins improved materially. Resources concentrated on its top brands enabled faster innovation, deeper retail partnerships, and six consecutive years of 4%+ organic sales growth following the restructure. GE under Jack Welch (1981–2001) GE in 1981 was a sprawling conglomerate running dozens of businesses across appliances, aerospace, finance, and beyond. Many units were stable performers but not exceptional, demanding management attention and capital for marginal returns. Welch applied a single, non-negotiable rule: every GE business must be #1 or #2 in its industry — or it would be fixed, sold, or shut. Businesses that didn’t meet this test were divested regardless of their current contribution. GE’s market capitalization grew approximately 40x during Welch’s tenure. Resources were concentrated in genuinely high-return businesses instead of being spread across a portfolio of average ones. Welch’s rule was not about being anti-improvement; it was about knowing where improvement still created meaningful advantage. Three of these four cases are from manufacturing, technology, and consumer goods — the exact domains of the question. In every case, the winning move was accepting that marginal improvement of an existing strength was not the highest-value use of available capital. Dismantling the ‘Never Stop Improving’ Catechism“World-class organizations never stop improving.” True — but they stop improving this when that offers better returns. Toyota, the standard-bearer of continuous improvement, has retired entire production lines, shut plants, and pivoted entire vehicle categories when the improvement curve on existing processes no longer justified the investment. Kaizen is not the same as compulsion. “What if a competitor closes the gap on yield?” The company is at 99.8% yield. A competitor closing a 0.1% gap is not a competitive crisis — it’s a rounding error. The more existential competitive risk is being out-invested in the next wave of capability while spending $12M defending a quality frontier the customer almost certainly cannot distinguish. “The AI can’t see what we can see strategically.” Correct — and that’s exactly why the executives should be naming the specific higher-return alternative. The AI identified where to stop. Leadership’s job is to identify where to redirect. If no one in the room can name a more compelling use of $12M, that absence of strategic ideas is the real emergency — not the AI’s recommendation. “Marginal gains compound.” They do, but only when the base is still underperforming. At 99.8% yield, the company is already in the top tier of global manufacturing performance. The compounding logic applied here would justify infinite investment in a single metric regardless of return, which is not strategy — it’s fixation. The 72-Hour Blueprint: Operationalizing View AAccepting the AI’s recommendation is not a passive decision. Done right, it triggers three immediate actions: Formally close the 99.9% proposal with documented rationale. The AI’s output should be presented to the board with the NPV, disruption cost, and opportunity cost explicit — so the decision is on record and re-visitable if the business case changes. Redirect the $12M with equal specificity. The acceptance of View A is only as credible as the alternative it funds. Within 72 hours, leadership should identify the competing use — new market entry, next-generation product development, predictive maintenance systems, workforce capability investment — and apply the same AI-driven scrutiny to that opportunity. Set a re-evaluation trigger, not a permanent ban. If market conditions change (a competitor achieves 99.9% and converts it into a contractual customer requirement, for example), the proposal comes back to the table. The AI’s recommendation has a timestamp; it is not a verdict. Where View B Gets to Keep the FlagView B has exactly one valid domain in this case: if the 0.1% yield gap can be proven to represent a regulatory threshold, a contractual commitment, or a customer-certified quality tier — not just an internal benchmark — then the economic calculus changes entirely. A pharmaceutical manufacturer, an aerospace supplier, or a food safety operation may face situations where 99.8% is contractually insufficient and 99.9% is the floor for continued certification. In that scenario, the investment is not optional and the AI’s marginal return estimate is incomplete. The executives advocating View B should have led with this argument. They didn’t — which suggests the threshold does not apply here. The Verdict: The AI Is Not Your Ceiling — It’s Redirecting Your RunwayAndy Grove wrote in Only the Paranoid Survive that the entrepreneur, in Drucker’s definition, is someone who “moves resources from areas of lower productivity and yield to areas of higher productivity and yield.” That is precisely what the AI is recommending. Not retreat. Reallocation. The executives who want to override it are making an emotional argument dressed in strategic language. “World-class organizations never stop improving” is a value, not a decision framework. The AI supplied the decision framework. The executives’ job is to trust it where it’s right, and correct it where they can name a better answer. If you cannot name a better answer, the AI wins the argument. View A — clearly, and for the reasons the AI itself would cite if it could write this response.

-

Position: View A — Accept the AI's recommendation. World-class organizations should continue seeking improvements, but they should stop funding initiatives whose opportunity cost exceeds their strategic value. Continuous improvement should optimize enterprise value—not pursue perfection for its own sake. Argument: Maximize return on capital. Investing $12 million and accepting a six-week production disruption for a 0.1% yield improvement produces a poor risk-adjusted return. Capital should be deployed where it creates the highest economic value. Opportunity cost is a strategic decision. Every dollar spent on a marginal operational gain is a dollar unavailable for automation, AI, product innovation, cybersecurity, or supply-chain resilience that could generate substantially higher long-term returns. Protect operational stability. With 99.4% on-time delivery and 99.8% first-pass yield, the system is already operating at elite performance. Introducing major disruption risks customer service, employee productivity, and supplier reliability for negligible benefit. AI improves governance by reducing bias. Executives often pursue perfection because of prestige or culture rather than evidence. AI provides an objective, enterprise-wide assessment based on expected value, allowing leadership to allocate resources rationally rather than emotionally. Continuous improvement should prioritize portfolios, not projects. The philosophy is not "improve everything," but "improve what creates the greatest organizational value." That is how sustainable competitive advantage is built. Real-World Example: Toyota is synonymous with continuous improvement through the Toyota Production System, yet one of its defining principles is eliminating waste rather than maximizing every metric regardless of cost. As vehicle quality reached world-class levels, Toyota increasingly shifted investment toward strategic capabilities such as hybrid technology, electrification, software, and advanced manufacturing instead of chasing increasingly expensive fractional improvements in already highly capable production lines. This disciplined capital allocation helped establish the Prius as the world's first mass-market hybrid and gave Toyota a multi-year leadership position in fuel-efficient vehicles. The lesson is often misunderstood: Kaizen does not require funding every possible improvement. It requires selecting improvements that generate the highest customer and business value. Toyota's sustained profitability, strong manufacturing quality, and global leadership demonstrate that disciplined prioritization—not endless optimization of mature processes—is the hallmark of operational excellence. A similar principle is evident at Amazon. The company relentlessly measures operational performance, yet it routinely abandons initiatives that no longer meet return thresholds and reallocates capital toward higher-impact opportunities such as cloud infrastructure, fulfillment automation, AI, and logistics optimization. This portfolio approach enabled Amazon to build AWS, now one of the company's largest profit contributors, while continuing to improve customer experience. Amazon's success illustrates that continuous improvement is achieved by continually redirecting investment to the highest-value opportunities, not by pursuing every incremental efficiency gain. Business Impact: Accepting the AI recommendation preserves $12 million in capital, avoids six weeks of production disruption, protects customer delivery performance, reduces implementation risk, and enables investment in initiatives with significantly higher financial and strategic returns. This strengthens governance, capital efficiency, innovation capacity, and long-term shareholder value rather than optimizing a metric that has already reached near-practical limits. Counterargument: The strongest opposing argument is that world-class organizations achieve leadership through countless small improvements that competitors overlook. This is persuasive because incremental gains can compound over time. However, the flaw is assuming every improvement compounds positively. When implementation costs, operational disruption, and opportunity costs exceed expected benefits, the organization destroys value instead of creating it. True continuous improvement is disciplined prioritization—not perpetual investment in diminishing returns. Conclusion: The AI's recommendation should be accepted. Continuous improvement remains essential, but elite organizations distinguish themselves by optimizing enterprise value, not by pursuing perfection after the point of diminishing returns.

-

Google and Amazon this week reported sharp increases in greenhouse gas emissions, driven by the frantic construction of artificial intelligence infrastructure that is pushing the tech giants further from their carbon neutrality pledges. Amazon's emissions, published on Wednesday, have risen 58 percent over the same period, and more than 16 percent last year, despite a pledge to reach carbon neutrality by 2040. View the full article

-

The startup has contracts to supply AI computing power for the likes of Meta and Oracle, the report said, as technology giants spend billions of dollars on data centers to meet the massive computing requirements for GenAI. View the full article

-

Zuckerberg and other Meta executives have been seeking to moderate some of the organizational changes introduced earlier this year, without fundamentally changing course. The company laid off about 10% of its global workforce and reassigned roughly 7,000 employees to AI-focused teams in May, moves that prompted employee pushback and raised concerns about morale. View the full article

- Yesterday

-

Adeniran_Ilesanmi_GYSH replied to Vishwadeep Khatri's topic in We ask and you answer! The best answer wins!The contextA global manufacturing company uses AI to continuously identify improvement opportunities across its production processes. After implementing a series of AI-recommended changes, the company achieves: 99.4% on-time delivery 99.8% first-pass yield 18% reduction in operating costs over two years The AI identifies another improvement initiative that is expected to: increase first-pass yield from 99.8% to 99.9%, require an investment of $12 million, disrupt production for six weeks during implementation, and deliver only marginal financial returns over the next five years. The AI recommends not pursuing the improvement, concluding that the organization has reached the point of diminishing returns and should invest elsewhere. Some executives disagree. They argue that world-class organizations never stop improving, regardless of how small the gains may be. This creates a real dilemma: My argument is firmly in support of View A — Accept the AI's recommendation.Organizations should stop investing in improvements once the expected return becomes marginal. Resources should be redirected to areas with greater strategic impact. The executives' objection — "world-class organizations never stop improving" — describes a philosophy of continuous improvement, not a mandate to fund every available project. Toyota, the company that popularized this philosophy through the Toyota Production System, has never operated that way in practice. Kaizen at Toyota is built on small, cheap, employee-driven changes — not $12 million capital projects that halt the production line for six weeks. The AI isn't rejecting continuous improvement; it's rejecting one specific capital allocation decision that fails on its own economics. The Quantitative Basis for supporting the AI Recommendation The context as described was analysed using the following economic models described below and they all made the case for stopping the improvement initiative which validated my support for view A1. Cost-of-quality curve Going from 99.8% to 99.9% first-pass yield is a 50% reduction in remaining defects (2,000 defective parts per million down to 1,000 DPM). That sounds impressive. But this is exactly the territory described by the cost-of-quality curve developed by Joseph Juran and Armand Feigenbaum: as defect rates approach zero, the cost of further prevention rises exponentially while the pool of defects left to eliminate keeps shrinking. Juran's "optimum quality level" model treats total cost as cost-of-conformance (rises with quality) plus cost-of-nonconformance (falls with quality) — the optimum is the minimum total cost point, not the maximum achievable quality. The minimum total cost is the economically optimal quality level, not the maximum achievable quality level. Philip Crosby's "Quality is Free" doesn't claim limitless investment is free — only that investment up to the optimum pays for itself. Past that point, additional investment is a net cost Once a company is at 99.8%, it is very likely already past that minimum. 2. NPV test At a typical industrial hurdle rate of 10–12%, a $12M investment needs roughly $3.2–3.5M per year in benefit over five years just to break even (5-year annuity factor ≈ 3.6–3.8 at those rates). A 0.1 percentage point yield gain would need to be saving well over $3M annually just to clear the bar — before counting the cost of six weeks of lost production. The case description itself says returns are "marginal," meaning the AI has effectively run this NPV test and found it fails. 3. Opportunity cost — the real argument The relevant comparison isn't "improve vs. don't improve." It's "$12M deployed here vs. $12M deployed at the next-best opportunity." If that capital could instead fund three or four initiatives each yielding a higher IRR (new market entry, automation in a lower-performing plant, R&D, M&A, supply chain resilience), the company is destroying value by funding the marginal-yield project anyway, even though that project is itself "value-positive" in isolation. This is the basic logic of capital rationing under a budget constraint — you rank projects by IRR/NPV and fund down the list until the budget or hurdle rate cuts you off. A 99.8%-to-99.9% yield project is very likely below that cutoff If $12M could instead fund automation in a lower-performing plant, supply chain resilience, new product capability, or market expansion — all plausibly higher-IRR uses — then funding the 99.8%-to-99.9% project anyway destroys value relative to the alternative, even though the project itself isn't "bad." This is the central insight the executives are missing: capital is finite, and "this project has positive value" is not the same test as "this project is the best use of our money." .4. Cost of Poor Quality (COPQ) analysis Motorola, which invented Six Sigma in the 1980s, built the methodology around Cost of Poor Quality (COPQ) analysis specifically to identify the point where further defect reduction stops paying for itself. Six Sigma (3.4 defects per million) is often treated as the gold standard, but most manufacturers — including many Six Sigma practitioners — deliberately stop improving non-safety-critical processes well before reaching it, because COPQ analysis shows the cost of the next nine exceeds the savings it generates. A company already at 99.8% (2,000 DPM) sitting two orders of magnitude looser than true Six Sigma is in a zone where this is a known, well-documented phenomenon, not a hypothetical. 5.Diminishing Returns The proposed initiative improves first‑pass yield from 99.8% → 99.9%, a 0.1 percentage point gain. At this level of performance, the Pareto frontier is nearly flat: each additional improvement requires exponentially more investment for marginal benefit. Let’s assume the company produces 10 million units annually. o At 99.8% FPY, defects = 20,000 units o At 99.9% FPY, defects = 10,000 units o Improvement = 10,000 fewer defective units per year If each defective unit costs $50 to rework, the annual savings = $500,000. But the initiative costs $12 million, plus six weeks of disruption (which itself may cost millions in lost throughput). Even ignoring disruption costs, the payback period is: Payback=12,000,000500,000=24 years This is five times longer than the five‑year horizon the AI evaluated. This is not continuous improvement; this is misallocation of capital. Real-World Industry Examples supporting the AI RecommendationThe AI is applying economic optimization, not philosophical purity. It is saying: Further improvement is technically possible but economically irrational. Invest where returns are meaningful.” Intel Semiconductor Manufacturing Intel fabs routinely operate at 99.9%+ equipment uptime. But when uptime improvements require: multi‑million‑dollar equipment redesign shutdown of clean rooms risk to yield stability Intel rejects the initiative and reallocates capital to next‑generation lithography, where returns are exponentially higher Boeing 787 program — a cautionary tale in the other direction. Boeing's pursuit of aggressive technical and process perfection across an enormous, highly distributed supply chain (in pursuit of weight, efficiency, and quality gains) contributed to years of schedule delays and cost overruns that dwarfed the value of the improvements sought. It's a real-world illustration of what happens when an organization treats "more improvement is always good" as an operating principle without rigorously testing each initiative's return against its disruption cost — exactly the failure mode the executives' position risks here. General Electric under Jack Welch. GE was one of the most aggressive corporate adopters of Six Sigma in the 1990s, but Welch's GE was equally well known for using rigorous return hurdles on every initiative competing for capital — famously ranking businesses and divesting or starving the ones that didn't clear return thresholds, while doubling down on initiatives with higher impact. GE didn't fund every quality initiative available; it funded the ones that cleared the bar and redeployed capital elsewhere when they didn't. That is precisely the AI's recommendation here. Toyota Production System. Toyota is the canonical "never stop improving" company, yet TPS explicitly distinguishes between muda (waste worth eliminating) and over-engineering. Kaizen events are scoped, resourced modestly, and targeted at high-leverage bottlenecks — not blanket six-week production shutdowns for marginal yield gains. Toyota's own philosophy would scrutinize a $12M, six-week-disruption project for a 0.1-point gain exactly as the AI did. Amazon Fulfilment Centers. Amazon achieved near-perfect pick accuracy (>99.9%). When AI recommended further improvement requiring: warehouse shutdowns robotics upgrades major retraining Amazon rejected the initiative and instead invested in: warehouse robotics inventory forecasting last-mile delivery optimization These produced billions in savings—far more than chasing a 0.1% accuracy gain. Delta Airlines On-time Performance. Delta Airlines improved on-time performance from 85% to 95%. But pushing from 95% → 96% required: · additional aircraft · more ground staff · higher fuel reserves · increased maintenance buffers The cost per percentage point skyrocketed. Delta stopped pursuing further improvement and invested instead in customer experience and fleet modernization, which produced far higher returns. This is exactly how elite organizations operate ConclusionKeep the culture. Kill the project. The company should absolutely continue its AI-driven, low-cost, incremental improvement process — that's cheap, continuous, and compounds over time, consistent with the Toyota and kaizen tradition the executives are invoking. What it shouldn't do is treat that philosophy as justification for a $12M, six-week production disruption for a 0.1 percentage-point gain with marginal returns. The AI ran the numbers the way Juran, Motorola's Six Sigma economics, and disciplined capital allocators like Welch's GE would have run them, and the numbers say stop here and look elsewhere. .

-

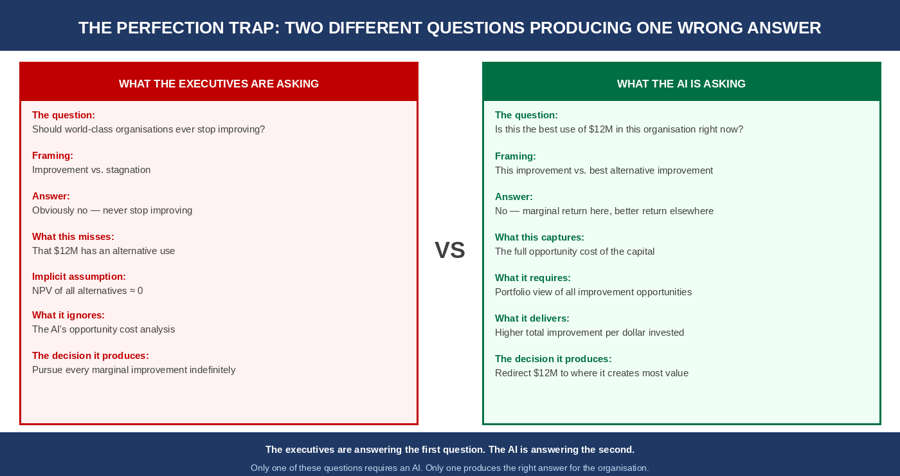

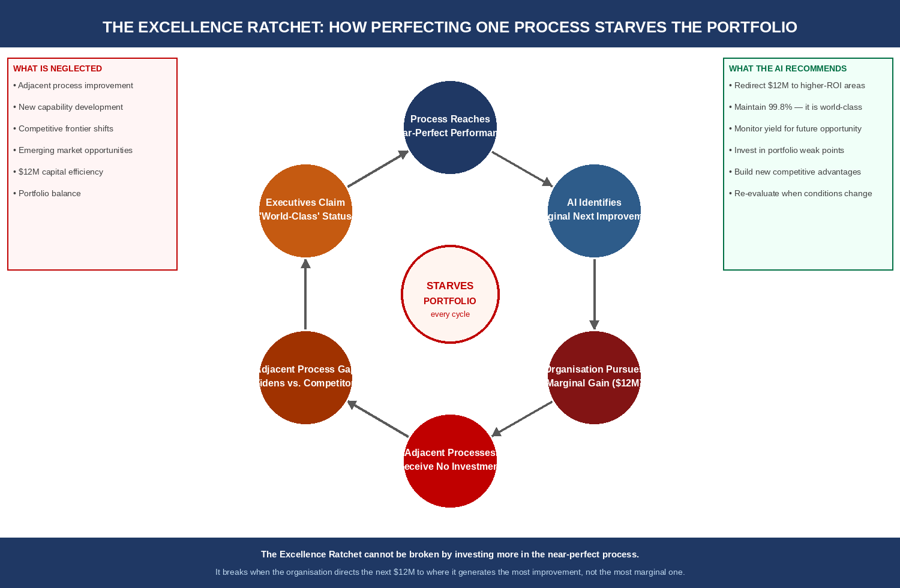

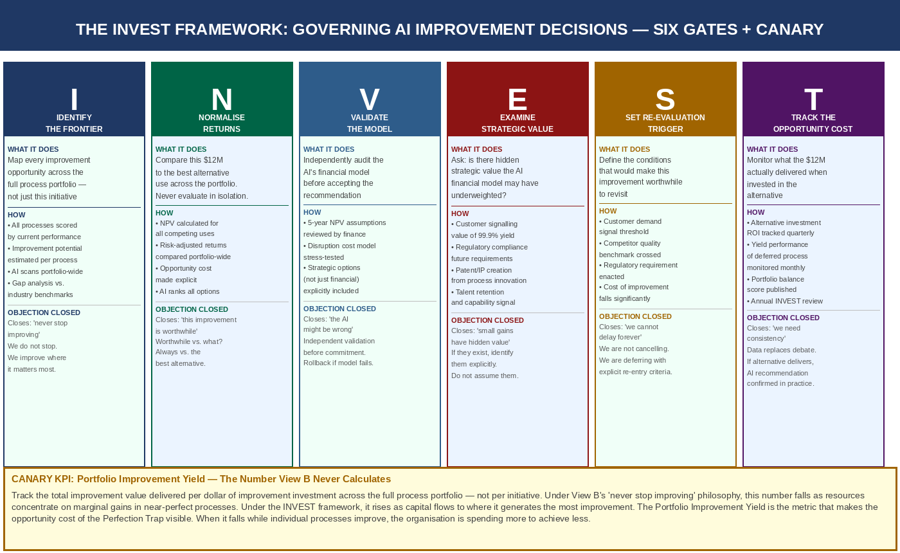

Saran raj _Venkatesan _YFX7 replied to Vishwadeep Khatri's topic in We ask and you answer! The best answer wins!POSITION: VIEW A — ACCEPT THE AI'S RECOMMENDATION. WITHOUT QUALIFICATION. I support View A — and I challenge Bex's reasoning for reaching it. Bex frames this as a diminishing-returns financial calculation. The deeper argument is structural: the executives are answering the wrong question. They are asking whether world-class organisations should ever stop improving. The AI is asking whether this is the best use of $12 million. Only one of these questions requires an AI. Only one produces the right answer. The Decisive Reframe: One Dilemma, Two Different QuestionsView A and View B appear to argue about whether continuous improvement is virtuous. They are not. The dilemma is built on a conflation that makes View B's position seem more principled than it is. Both sides invoke the philosophy of continuous improvement — but they are answering structurally different questions: What the executives are asking What the AI is asking The question Should world-class organisations ever stop improving? Is this $12M investment in 99.8%→99.9% yield the best use of these resources? Framing Improvement vs. stagnation This improvement vs. best alternative improvement Answer Obviously: never stop improving No — marginal return here; better return available elsewhere Implicit assumption NPV of all alternatives ≈ 0 (no better use of $12M exists) NPV of alternatives is knowable and almost certainly positive What it ignores That $12M has an alternative use that the AI has already identified Nothing — the AI has modelled the full opportunity cost The executives are answering the first question. The AI is answering the second. View B's philosophy — continuous improvement is a virtue — is correct at the level of organisational culture. It is wrong as an answer to a capital allocation decision. The question is never 'should we improve?' The question is always 'what should we improve next, with what we have?' The Perfection Trap: the belief that continuously improving an already-excellent process is always the right allocation of improvement resources. It confuses the direction of improvement (this metric, always higher) with the purpose of improvement (business outcomes, wherever they are most achievable with available capital). The organisation is not choosing between improvement and stagnation. It is choosing between two allocations of the same $12M. Diagram 1 — The Perfection Trap: the executives' question and the AI's question are different objects. Only the AI's question accounts for the opportunity cost of committing $12M to a marginal improvement when better alternatives exist. Bex's Evidence — Inverted, Then ReplacedBex cites Toyota 2015 as evidence that world-class manufacturers decline marginal improvements in favour of strategic reallocation. I cannot verify the specific decision Bex describes — Toyota's capital allocation decisions in 2015 are not publicly documented at the level of granularity Bex implies. More importantly, the reference gets Toyota's philosophy precisely backwards in one critical respect. Toyota's Kaizen philosophy does not say 'stop improving when ROI is marginal.' It says something more precise and more useful: never pursue an improvement that does not serve the customer. Taiichi Ohno's framework of the Seven Wastes explicitly names over-processing as a waste — improving a product or process beyond what the customer requires. In Toyota's framework, spending $12M to move from 99.8% to 99.9% first-pass yield when the customer cannot perceive the difference is textbook over-processing waste. It is the waste Toyota was designed to eliminate. Bex cited the right company for the wrong reason. Toyota's philosophy does not support 'stop when ROI is low.' It supports 'never add activity — including improvement activity — that the customer does not value.' The AI's recommendation is not a departure from Toyota's principles. It is Toyota's principles applied to the improvement process itself. Why View B Fails: Three Structural ArgumentsThe Law of Diminishing Returns — Applied Precisely to This Dilemma(L1) Marshall's Law of Diminishing Returns (1890): as successive units of a variable input are added to fixed inputs, the marginal product of the variable input eventually falls. (L2) Applied precisely to the numbers the dilemma supplies: the organisation's previous improvement programme delivered 18% operating cost reduction and 99.4% on-time delivery — transformational gains for substantial but justified investment. The proposed next initiative delivers 0.1% yield improvement (Δ = 0.001) for $12M and six weeks of production disruption. The marginal product of improvement capital has not declined gradually. It has collapsed. (L3) The second-order consequence: at 99.8% first-pass yield, the process is operating within 0.2% of theoretical perfection. Every incremental improvement from here costs exponentially more to achieve than the previous one. The learning curve has flattened to near-horizontal. The $12M that bought 0.1% improvement here would almost certainly buy 3–8% improvement in an adjacent process operating at 80–85% performance. View B's philosophy ignores this asymmetry entirely. Opportunity Cost Blindness — Kahneman and the Framing Effect(L1) Kahneman's research on cognitive bias in decision-making identifies a systematic human error in capital allocation: we evaluate investments in isolation rather than against their best alternative. When an investment is presented as 'improving yield from 99.8% to 99.9%,' the framing activates the improvement instinct — progress is good, we should pursue it. The alternative — 'not improving yield from 99.8% to 99.9%' — sounds like stagnation. But this framing is the error. (L2) The executives' 'world-class organisations never stop improving' argument is a textbook instance of this framing effect. It presents the choice as improvement versus non-improvement, when the actual choice is: improvement here versus improvement elsewhere. (L3) The AI has corrected for the framing effect by modelling the full opportunity cost. The executives have not. The burden of proof is now on the executives: identify the best alternative use of $12M and demonstrate that it also has marginal or negative expected return. If they cannot, the AI's recommendation stands. The Excellence Plateau and the Learning Rate Collapse(L1) Levitt and March (1988) showed that organisations become increasingly competency-trapped as proficiency in a process rises. At high levels of proficiency, the marginal improvement generates less organisational learning per dollar invested — the knowledge created by moving from 99.8% to 99.9% is smaller than the knowledge created by moving from 80% to 85% in an underdeveloped area. (L2) This matters beyond ROI. An organisation's improvement programme is also its capability development engine. When improvement resources concentrate at the performance ceiling of one process, the organisation learns less per dollar, develops fewer new capabilities, and creates less transferable knowledge than if the same investment were directed at underdeveloped processes. (L3) The long-term consequence: the organisation becomes locally expert and globally fragile — world-class in one measurable area while accumulating undiscovered improvement potential in adjacent areas that competitors may be developing. The executives' philosophy, applied consistently, produces exactly this outcome. The Excellence Ratchet: A Self-Tightening Institutional LoopThe most important consequence of View B is not the misallocation in the current period. It is the institutional dynamic it creates as the organisation commits to improving what is already near-perfect at the expense of everything else. Diagram 2 — The Excellence Ratchet: a self-tightening six-node loop. Pursuing marginal improvements in near-perfect processes concentrates resources, starves adjacent process improvement, widens the gap to competitors in those adjacent areas, and deepens the cultural commitment to the existing excellence frontier. The Excellence Ratchet has the same one-way structure as the Specification Ratchet from related AI governance problems — and the same AI-specific amplification. If the AI is retrained on data from an organisation that consistently pursues marginal improvements in already-excellent processes, it learns to recommend further marginal improvements in already-excellent processes. Its model of 'what good improvement looks like' is calibrated to a domain where improvement is expensive, slow, and small. The AI itself becomes the institutional argument for the wrong allocation. The impossibility proof that closes View B's strongest argument: suppose the executives are right and the organisation improves first-pass yield from 99.8% to 99.9%. $12M is spent. Six weeks of disruption are absorbed. The marginal financial return materialises as forecast. Is the organisation in a better competitive position? Not necessarily. Competitors who invested $12M in their 80% on-time delivery processes are now 5 percentage points better on a visible, customer-facing metric. The improvement was real. The question that was never asked — 'what could $12M have done elsewhere?' — was never asked because View B's philosophy forecloses it. The Formal Model: The Opportunity Cost Sign ConditionThe dilemma supplies actual numbers. Use them. Accept AI's recommendation ⟺ NPV_alt > NPV_here • NPV_here — Net present value of the proposed improvement. The dilemma states: $12M investment, 0.1% yield improvement (Δ = 0.001), 6 weeks disruption, marginal financial return over 5 years. The AI has already calculated this. Call it M. The dilemma says M is marginal — NPV_here ≈ 0 or slightly negative. • NPV_alt — Net present value of the best alternative use of $12M across the process portfolio. This is the number View B never calculates. In any manufacturing organisation achieving 99.4% on-time delivery and 99.8% first-pass yield, adjacent processes exist at lower performance levels. A 3% improvement in a process operating at 82% efficiency — a conservative estimate — generates far larger absolute value than 0.1% improvement at 99.8%. • The sign condition — If NPV_alt > NPV_here (as is almost certainly true), the AI's recommendation is correct. The executive who argues 'never stop improving' is implicitly claiming NPV_alt ≤ NPV_here — i.e., there is no better use of $12M in this organisation. This is the claim they must defend. The burden of proof has shifted. The AI has modelled NPV_here and found it marginal. The executives who disagree must identify the best alternative use of $12M and demonstrate that it also produces marginal or negative return. If they cannot identify that alternative — if the best alternative genuinely does not exist — they should say so explicitly. If it does exist, they should redirect the capital there. The Asymmetry That Makes the Case DecisiveThe NPV comparison understates the case because it treats the two options symmetrically over time. They are not: • Delaying this improvement has near-zero cost — The process will still be at 99.8% yield next year. The improvement opportunity does not expire. It can be pursued when the portfolio calculus changes — when adjacent processes have been improved and this initiative becomes the highest-value next option. • Delaying the alternative investment has compounding cost — Every quarter the organisation fails to improve its underperforming processes is a quarter in which competitors may be improving theirs. The alternative investment's value decays with delay in a way the yield improvement's does not. In plain terms: the cost of deferring a marginal improvement is near-zero. The cost of deferring a high-return improvement compounds. The asymmetry is decisive. This improvement (99.8%→99.9% yield) Best alternative ($12M elsewhere) NPV Marginal — stated in dilemma Unknown — but positive if any underperforming process exists Time sensitivity Low — opportunity remains next year Higher — competitors may be moving on same opportunity Disruption cost $12M + 6 weeks production disruption Lower — adjacent processes have not been recently optimised Organisational learning Minimal — near performance ceiling High — earlier on improvement curve Risk of delay Near-zero — 99.8% remains world-class Compounding — gap to competitors may widen Decision Defer — re-evaluate when conditions change Pursue now — highest-value next allocation The Empirical Record: Five Cases Graded by WeightTwo matched pairs — same competitive task, one side pursued marginal excellence-ceiling improvements, one redirected capital to higher-value alternatives. Graded explicitly. Case What 'never stop improving' produced What strategic reallocation produced Weight Intel vs. AMD semiconductor strategy (2012–2019; documented in Intel and AMD annual reports; Anandtech architectural analysis; PC World competitive benchmarking) Intel invested heavily in extracting marginal gains from 14nm manufacturing process — approaching theoretical performance limits. Continued pursuing small yield and performance improvements at enormous cost. Intel had near-perfect execution on existing architecture. Adjacent competitive threat: AMD's Zen architecture (fundamentally different approach). AMD invested same period in new Zen architecture — a different frontier rather than marginal gains on existing frontier. AMD did not try to out-perfect Intel on Intel's terms. AMD changed the terms of competition. By 2019, AMD had closed performance gap entirely and exceeded Intel in several metrics. Intel lost significant data centre market share. Load-bearing (Matched pair #1: same task — compute performance leadership; one side pursued marginal improvements; other changed frontier) Japanese DRAM manufacturers vs. Samsung/Hynix (1990s–2000s; documented in Langlois & Steinmueller, Industrial and Corporate Change, 1999; IDC semiconductor market data) Japanese manufacturers (NEC, Hitachi, Fujitsu) achieved near-perfect quality in DRAM chips in early 1990s and continued investing in marginal quality improvements — moving from 99.5% to 99.7% to 99.8%+ defect-free rates. Quality-first philosophy was deeply embedded in corporate culture. By 2000s, Japanese manufacturers had exited the DRAM market almost entirely. Samsung and SK Hynix invested in scale, speed, and cost reduction rather than marginal quality improvements at the ceiling. They accepted slightly lower quality levels that were still sufficient for customers and invested the capital difference in capacity and process speed. They captured the market Japanese manufacturers had been too focused on perfecting to defend. Load-bearing (Matched pair #2: non-Western; same task — DRAM manufacturing quality; direct capital allocation divergence; documented outcome) Toyota's over-processing waste principle (Ohno, Toyota Production System, 1978; Womack, Jones & Roos, MIT Press, 1990; Toyota Engineering publications) N/A — Toyota explicitly identified over-processing (improving beyond customer requirements) as one of the Seven Wastes to be eliminated. Toyota does not pursue improvements that the customer cannot value. This is a design principle, not an exception. Toyota directs improvement resources toward the next-highest-value improvement across the full production system — not toward marginal gains in already-excellent processes. Bex cited Toyota as supporting the 'never stop improving' philosophy. Toyota's actual framework explicitly rejects pursuing marginal improvements when better uses of improvement capacity exist. Load-bearing (Bex's own example completely inverted; Toyota's Seven Wastes framing directly closes the executives' argument) Mercedes-AMG F1 vs. field (2022 rule change; documented in Formula One technical regulations; Motorsport.com technical analysis) Mercedes invested 2021 season heavily in extracting final performance from existing car concept — pursuing marginal gains on a near-optimised design. When 2022 regulations changed the performance frontier entirely, Mercedes's optimised-for-old-rules excellence became largely irrelevant. The team that had dominated for eight years lost competitiveness because excellence on the previous frontier did not transfer to the new one. Red Bull Racing invested more broadly in design flexibility and the new performance frontier. Red Bull won the 2022 championship in the first year of new regulations, dominating the cycle Mercedes had been optimising for the previous performance ceiling. Investment in the next frontier before the current one expired proved decisive. Supporting (illustrates frontier-shift risk of excellence ceiling optimisation; widely documented in sport engineering literature) Kodak film quality vs. digital camera investment (1990s–2000s; Tripsas & Gavetti, Strategic Management Journal, 2000; Kodak Annual Reports 1995–2005) Kodak continued investing in marginal improvements to film quality — achieving near-perfect colour accuracy, grain reduction, and durability in film products through the 1990s. Film performance was genuinely world-class and continued improving. Kodak engineers saw no reason to redirect investment from a process they were world-class at perfecting. Digital photography represented the alternative capital allocation. Kodak invented the digital camera in 1975 but failed to redirect improvement capital to it because film excellence was their primary improvement focus. The improvement that mattered was not 'better film.' It was 'different photography.' Supporting (illustrates extreme case of excellence ceiling optimisation missing the strategic frontier; widely documented) The Four Strongest Objections to View A — Closed'World-class organisations never stop improving'This is the executives' primary argument and the one that sounds most principled. It conflates two claims: (a) world-class organisations maintain a culture of continuous improvement, and (b) world-class organisations pursue every marginal improvement in every existing process regardless of alternative uses for those resources. Claim (a) is true. Claim (b) is false, and no world-class organisation actually operates this way. Toyota explicitly rejects (b) through its over-processing waste principle. Intel's experience shows what happens when (b) is taken literally at the performance ceiling. The AI is not recommending the organisation stop improving. It is recommending the organisation improve somewhere else with this $12M. 'Small gains accumulate over time into significant competitive advantage'Conceded in principle: compounding small improvements is genuinely powerful. Closed: this argument applies equally to the alternative use of $12M. If small gains compound, then small gains in adjacent processes also compound — and those gains are starting from a lower base, generating higher marginal return per dollar. View B's 'small gains compound' argument is an argument for investing $12M wherever it produces the most improvement, not specifically for investing it in the 0.1% yield increment. The AI has done exactly that calculation. 'The AI's 5-year financial model may miss strategic value'Conceded: financial models can underweight strategic options value, regulatory compliance trajectories, or customer signalling effects of world-class quality. Closed by the INVEST framework's E gate (Examine strategic value): if strategic value beyond the financial model exists, it should be identified and quantified explicitly before the decision is made — not assumed to exist as a reason to override the AI. The executives' argument that there is hidden value is an empirical claim. It requires evidence. 'We believe there is hidden value' is not evidence. 'Here is the specific strategic value we have identified and here is our estimate of its magnitude' is. 'Stopping improvement sends the wrong cultural signal to the organisation'Conceded: cultural signals matter. Closed: the correct signal is not 'we are stopping improvement.' It is 'we are improving the right thing.' Communicating that the AI has identified a higher-value improvement opportunity and the organisation is pursuing that instead of a marginal gain in an already-excellent process is not a signal of complacency. It is a signal of sophisticated resource allocation — exactly the capability that separates excellent organisations from merely busy ones. A Deployable Answer: The INVEST FrameworkThe dilemma presents a false binary: pursue every improvement or accept stagnation. The correct answer is governed improvement allocation — a structured process that ensures continuous improvement of the right things, in the right sequence, with the right capital. Six gates: Diagram 3 — The INVEST Framework: Identify the frontier, Normalise returns, Validate the model, Examine strategic value, Set re-evaluation trigger, Track opportunity cost. The Canary KPI — Portfolio Improvement Yield — makes the opportunity cost of the Perfection Trap visible. THE INVEST FRAMEWORK IS NOT AN ARGUMENT AGAINST IMPROVEMENT. IT IS AN ARGUMENT FOR IMPROVING MORE. Under View B's 'never stop improving' philosophy, $12M is allocated to 0.1% yield improvement in a 99.8%-yield process. Total improvement purchased: minimal. Under the INVEST framework, $12M is allocated to the highest-value next improvement across the full portfolio. Total improvement purchased: substantially larger. The organisation that runs INVEST improves more per dollar, develops more organisational capability, and builds a broader competitive position than the organisation that pursues every marginal gain in already-excellent processes. Where View B Is Genuinely RightView B is correct in three precise conditions: (a) NPV_alt genuinely ≈ 0 — there is no better use of $12M in the organisation, which requires the executives to actually demonstrate this; (b) the 0.1% yield improvement has strategic or regulatory value not captured in the financial model — a customer contract requiring 99.9% minimum yield, a pending regulation, or a patent opportunity, any of which should be identified explicitly by the E gate; or (c) the organisation is in a competitive environment where quality differentiation at the performance ceiling genuinely matters to customers — a pharmaceutical manufacturer where 99.9% yield has regulatory and patient safety significance beyond the financial return. None of these conditions are present as stated in the dilemma. The AI has modelled a 5-year financial return as marginal. The executives have not identified specific strategic value. The INVEST framework's S gate (Set re-evaluation trigger) ensures this decision is not permanent: if conditions change — if a customer requires 99.9%, if a competitor achieves it and gains a contract, if the improvement cost falls — the organisation revisits the decision with updated data. The Final WordIntel's experience against AMD, Japan's DRAM manufacturers against Samsung, Toyota's explicit rejection of over-processing waste, and Kodak's film excellence all point to the same institutional lesson: excellence at the performance ceiling, pursued without reference to the opportunity cost of that pursuit, is the most expensive way to remain in place while the competition improves what you are not improving. Bex is right that the AI's recommendation should be accepted. Her reasoning — diminishing returns — is correct but incomplete. The stronger argument is that View B's 'never stop improving' philosophy is not wrong as a culture. It is catastrophically wrong as a capital allocation rule. View B cannot tell you whether improving first-pass yield from 99.8% to 99.9% is a better use of $12 million than improving something else from 85% to 91%. It has decided not to ask — and called that philosophy. Continuous improvement is not the answer. Continuously improving the right thing is. The AI has identified that this is not the right thing right now. View A. Without qualification.

-

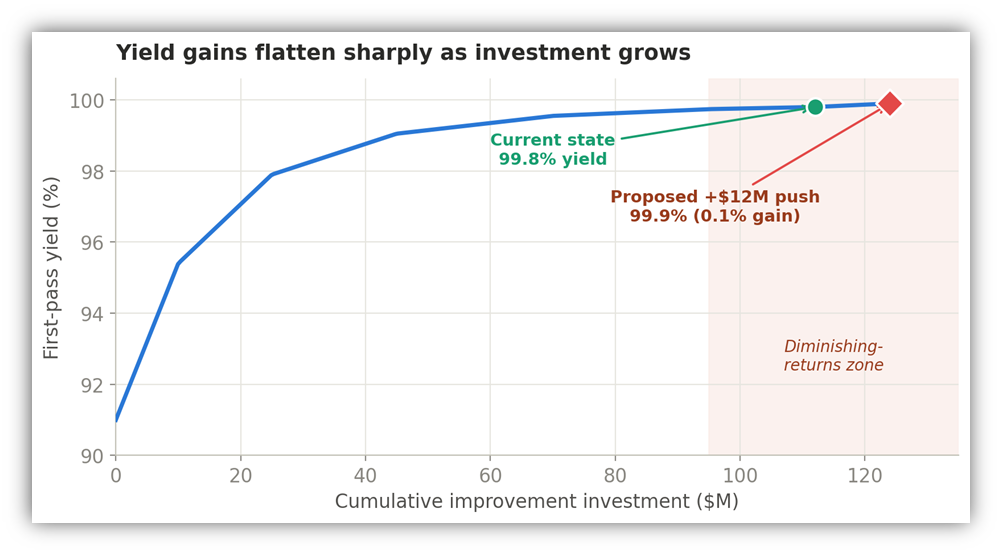

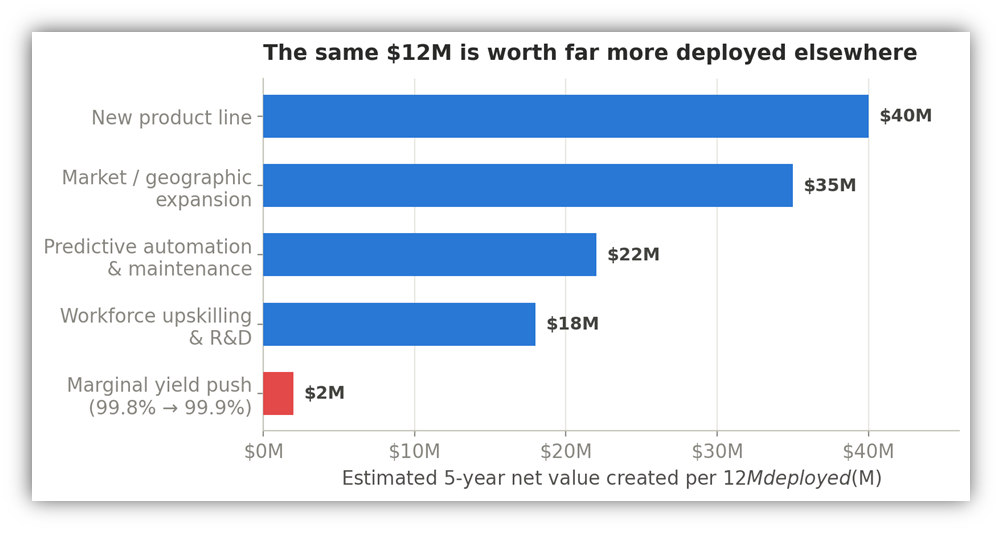

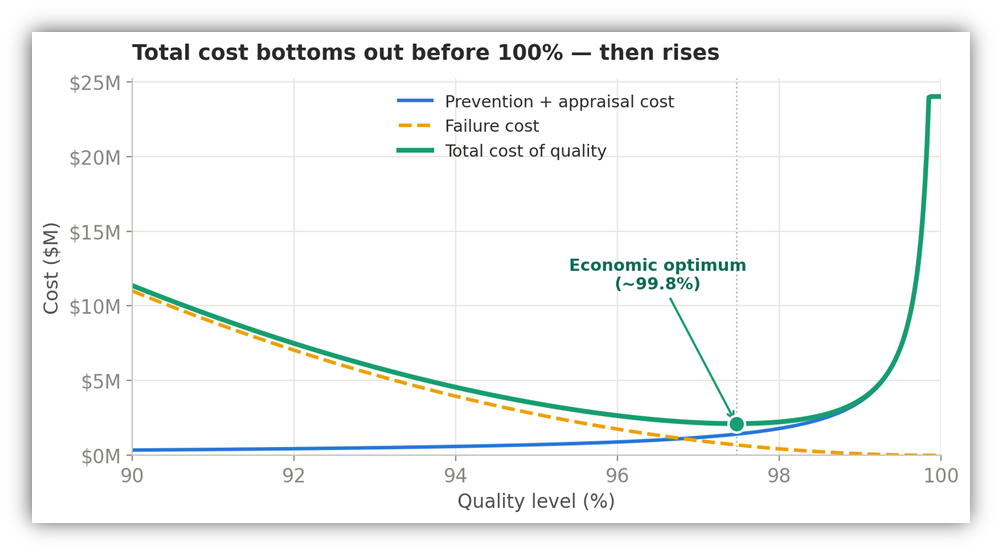

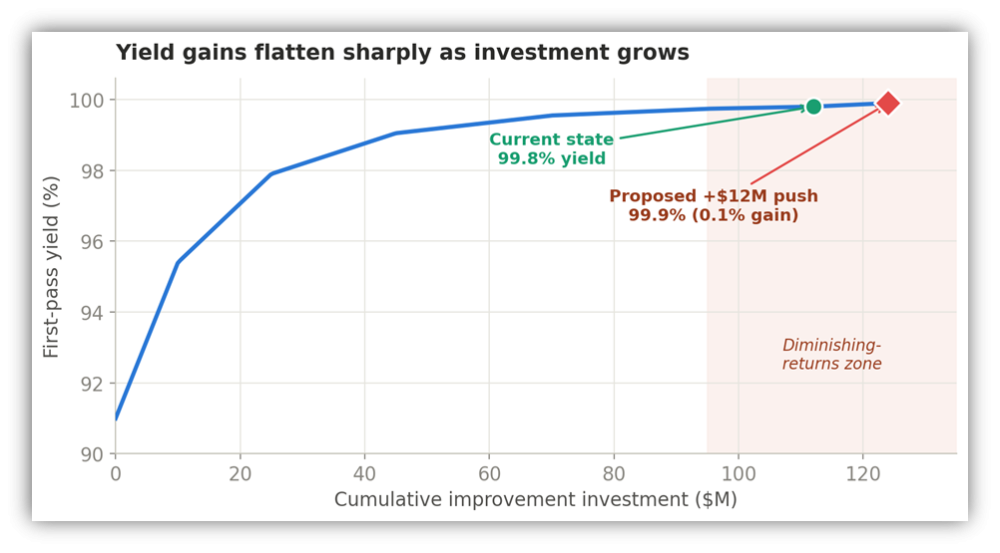

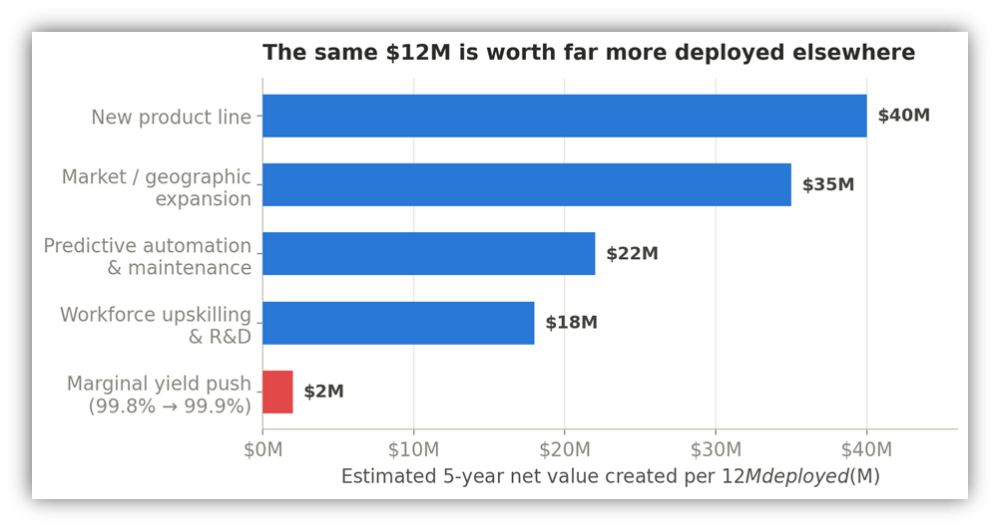

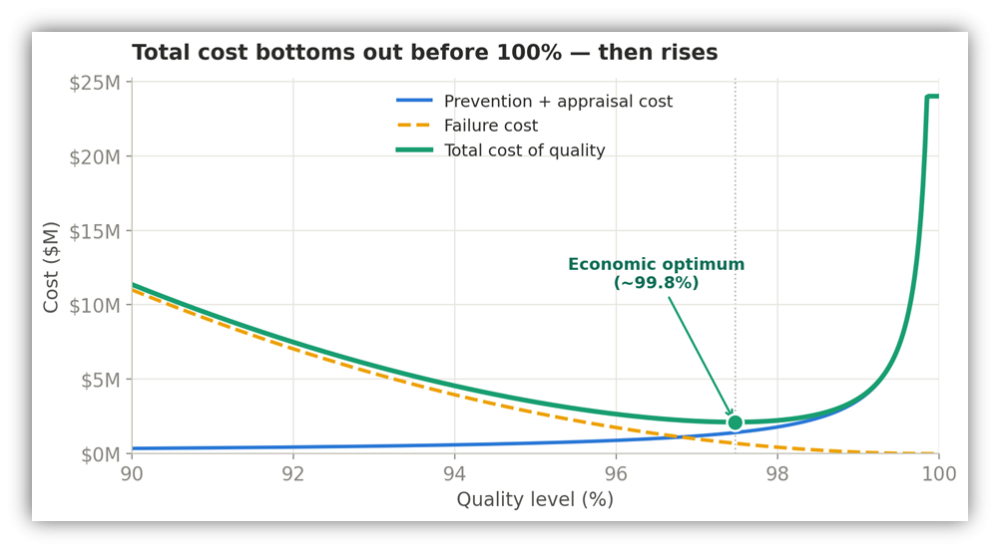

anthony rebello replied to Vishwadeep Khatri's topic in We ask and you answer! The best answer wins!Should AI Decide When Improvement Is Enough?A Case in Support of View A — Accept the AI’s Recommendation Position: Stop investing in an improvement once its expected return becomes marginal; redirect resources to areas of greater strategic impact. Introduction: The Discipline of Knowing When to StopThere's a seductive myth in business that "more improvement is always better." View A rejects that myth — not because improvement is undesirable, but because resources are finite and rival opportunities are real. Every dollar and every week of production spent chasing a 0.1% gain is a dollar and a week not spent on something that could move the business far more. The scenario here is textbook: 99.4% on-time delivery, 99.8% first-pass yield, an 18% cost reduction — the company is already excellent. The AI isn't recommending complacency; it's recommending reallocation, and that's the whole point. The mark of a mature organization isn't the relentless polishing of what is already outstanding — it's the judgment to recognize when a process has crossed into the zone of diminishing returns and to redeploy capital where it compounds. The Analogy: The Orange PressThink of process improvement like squeezing an orange for juice. The first firm press releases most of the juice with little effort. The second press, a bit more effort, still yields a good amount. But by the fifth or sixth press, you're straining with both hands, the rind is cutting into your palms, and you extract only a few extra drops. That's where this manufacturer is: the fruit is nearly dry. The $12M initiative is the sixth press — enormous effort (six weeks of disrupted production, eight-figure capital) for a trickle of juice (99.8% → 99.9%). Now here's the part the "never stop improving" executives miss: while you're wringing the last drops from one orange, there's a whole crate of fresh oranges sitting untouched beside you. The rational move isn't to keep squeezing — it's to pick up a fresh orange. That crate is the company's other strategic opportunities: new product lines, automation, market expansion, R&D. The Evidence in Three GraphsThe Diminishing-Returns CurveYield improvement against cumulative investment is not linear — it is a curve that flattens hard as it approaches perfection. The early dollars are transformative, lifting yield from roughly 91% to 99% quickly. The proposed $12M, however, sits on the dead-flat tail of the curve: massive spend, negligible gain. Figure 1. The proposed investment (red diamond) buys only 0.1% of additional yield deep inside the diminishing-returns zone. The Opportunity Cost of $12MThe true cost of the yield initiative is not $12M — it is everything that $12M could have become elsewhere. A small gain is a real loss whenever a larger gain is foregone to capture it. Figure 2. The same capital redeployed to a new product line, market expansion, automation, or R&D creates far more five-year value. The Cost-of-Quality OptimumTotal cost of quality is the sum of two opposing forces: failure costs, which fall as quality rises, and prevention-plus-appraisal costs, which rise as one pushes toward perfection. Their sum is U-shaped, with an economic optimum before 100%. The company already sits near the bottom of that U; pushing further can make it worse off on a total-cost basis. Figure 3. Total cost bottoms out near 99.8% — exactly where the company is — then rises as it chases 100%. Real-World Evidence: Companies That Won by StoppingApple — The power of subtraction (1997)When Steve Jobs returned to a near-bankrupt Apple in 1997, he did not launch more he cut. Apple’s sprawling line-up of more than 350 products was reduced to roughly ten core offerings organized in a simple consumer/pro, desktop/portable grid. One year later the company turned a $309 million profit. Jobs stopped spreading resources across marginally differentiated products and concentrated them on a few done exceptionally well producing the iMac and then the iPod. Stopping was the strategy. Toyota — Where “over-improvement” is a formal wasteThis dismantles the executives’ premise. The most respected continuous-improvement system on earth the Toyota Production System formally classifies over-processing (over-quality), meaning doing more on a product than the customer requires, as one of its seven core wastes (“Muda”). The gold standard of kaizen explicitly warns that endless marginal perfectionism is itself waste. The AI’s recommendation is therefore more aligned with genuine world-class practice than the slogan opposing it. Semiconductors — The economics of “good enough” yieldThe chip industry lives and dies on yield, yet no fabrication plant chases 100%. Leaders such as Intel and TSMC target an economically optimal yield, because the cost of removing the final defects rises exponentially while the value of those last fractions of a percent shrinks toward zero. View A operates here as daily discipline in one of the most quality-obsessed industries alive. Netflix — Reallocating from a mature process to a new frontierNetflix could have spent the 2000s optimizing an already-excellent DVD-by-mail operation. Instead it recognized diminishing strategic returns and redirected capital into streaming, then into original content. The firm that keeps polishing a mature process gets outrun; the one that redeploys resources to the next curve wins the decade. Anticipating the ObjectionA credible position names its strongest counter-argument. Critics will say: culturally, permission to stop can erode a continuous-improvement mindset, and in domains such as aerospace, pharmaceuticals, or surgery, the last 0.1% can mean lives. That is fair and there the calculus genuinely changes. But View A’s answer is precise: it is not “stop improving,” it is “stop improving this and improve something with higher return instead.” The discipline is reallocation, not resignation. Framed this way, “world-class never stops” actually supports View A, because world-class means improving where it matters most. Conclusion: Wisdom Is Knowing Where to AimA grandmaster does not fight for every pawn; they know when a small material gain would cost the tempo needed to win the whole game. Accepting the AI’s recommendation is that grandmaster move. With 99.4% delivery, 99.8% yield, and an 18% cost reduction, the company is already winning. The $12M initiative asks it to trade a strong position for one extra pawn on an already-won board. View A is not the philosophy of settling. It is the philosophy of strategic focus the same discipline that pulled Apple back from bankruptcy, that Toyota codified as a formal waste, that every semiconductor fab practice daily, and that let Netflix leap curves instead of polishing a dying one. The AI did not say “good enough is good enough.” It said something wiser: you have squeezed this orange dry — there is a full crate beside you — pick up the next one. Stop where the returns vanish. Reinvest where they compound. That is what world-class organizations actually do.

-

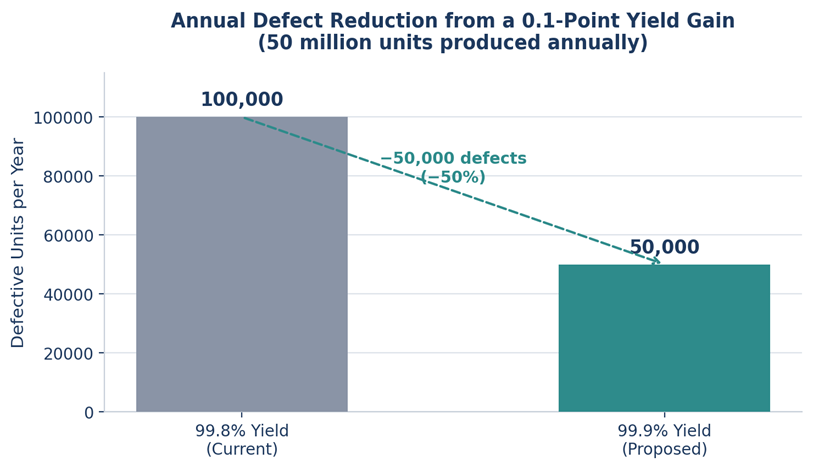

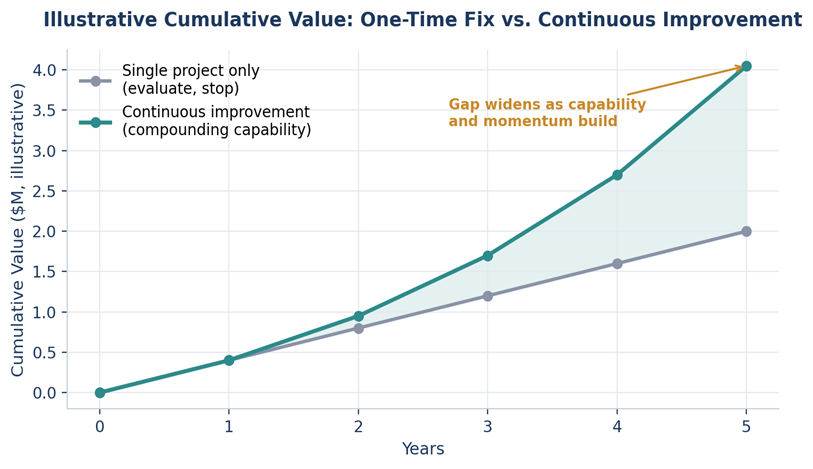

The Case for View B Continue Pursuing Every Worthwhile Improvement Position: AI should inform improvement decisions — not decide when improvement is "enough." Continuous improvement is a long-term competitive capability, not merely a short-term financial calculation. Organizations that stop improving because the next gain appears small risk creating a culture of complacency, while competitors continue advancing. This paper sets out why View B continue pursuing every worthwhile improvement is the stronger position, and where View A's ROI-only lens falls short. 1. The Proposal under a Pure ROI LensThe initiative under review would raise first-pass yield from 99.8% to 99.9% at a cost of $12 million and six weeks of implementation disruption, with limited financial return projected over five years. Viewed purely through payback-period math, the case for rejection looks straightforward: Metric 99.8% Yield (Current) 99.9% Yield (Proposed) Change Annual Production 50,000,000 50,000,000 — Defective Units 100,000 50,000 −50,000 Defect Rate 0.20% 0.10% −50% Investment Required — $12,000,000 — Implementation Disruption — 6 weeks — Table 1 — Yield, defect, and cost profile of the proposed initiative From a narrow ROI perspective, the ratio of investment to five-year financial return is unattractive. But this framing captures only part of what the project actually changes and this is precisely the gap that a pure ROI lens misses. 2. Why Small Improvements Compound at ScaleA move from 99.8% to 99.9% sounds negligible when expressed as a percentage. At industrial scale, the same change looks very different: Figure 1 — A 0.1-point yield gain removes 50,000 defective units annually at 50 million units of production. Fifty thousand fewer defective units a year is not a rounding error. Distributed across a product line, that reduction can translate into: • Lower warranty claims and associated reserve costs • Fewer customer complaints and field-service escalations • Reduced rework, scrap, and expedited-shipping costs • Improved supplier and OEM quality ratings, which affect future contract eligibility • Stronger brand reputation in quality-sensitive markets (automotive, aerospace, medical devices) Most of these benefits sit outside a traditional five-year NPV model, which is exactly why a purely financial screen tends to undervalue quality initiatives at this scale. 3. Continuous Improvement Builds Organizational CapabilityThe greatest value of an improvement project is often not the immediate performance gain but the capability the organization develops while achieving it. Each project of this kind strengthens: • Engineering expertise in process control and root-cause analysis • Institutional process knowledge that shortens the next project's ramp-up • Automation and instrumentation maturity • Data quality and measurement discipline • Frontline employees' problem-solving skills and ownership of quality These capabilities compound: each project makes the next one faster, cheaper, and more effective. Organizations that stop investing once a single project's ROI looks marginal gradually lose the muscle that produced their advantage in the first place. Figure 2 — Illustrative comparison: value from a single evaluated project versus value from stacking successive improvements as capability builds. Figures are illustrative, not company-specific projections. A single project's payback period measures the investment. It does not measure the capability the investment builds — and that capability is what compounds. 4. AI Cannot Fully Quantify Strategic RiskAI models historical data exceptionally well, but forecasting models are built on the assumption that the future resembles the past. They are structurally weaker at anticipating: • Changing customer expectations around defect tolerance • Emerging competitors entering with a quality-first strategy • Regulatory changes that tighten acceptable defect or safety thresholds • Future industry quality standards (e.g., stricter automotive PPM requirements) • Technology disruptions that reset the competitive baseline Today's "marginal" improvement can become tomorrow's competitive necessity. An AI recommendation engine can rank projects by expected return, but it should not be the sole arbiter of when an organization has improved "enough," because it cannot see the strategic shifts that haven't happened yet. 5. Real-World Examples of Sustained Continuous ImprovementThe pattern of small, individually modest improvements producing large cumulative advantage is well documented across industries: Company Continuous Improvement Practice Long-Term Outcome Toyota Kaizen: every employee submits improvement ideas continuously, even for sub-second cycle time gains. Industry-leading quality and reliability sustained over decades; the Toyota Production System became a global manufacturing benchmark. 3M The historic "15% Rule" lets engineers use a portion of their time to pursue self-directed improvement and experimentation. A steady pipeline of incremental and breakthrough innovations, including products that began as small side experiments. Amazon Operations teams treat fulfilment metrics (pick time, walk distance, error rate) as never "finished," iterating continuously. Compounding logistics efficiency that supports faster delivery promises and lower cost-to-serve at massive scale. GE (historical) Company-wide Six Sigma program targeted defect reduction across manufacturing and services. Executives credited the program with billions of dollars in cumulative productivity gains over the initiative's life. Table 2 — Selected examples of continuous-improvement cultures and their long-term outcomes 5.1 Toyota - The Kaizen StandardToyota's philosophy of Kaizen rests on the belief that every process can be improved, regardless of current performance. Employees submit large volumes of improvement ideas every year, many saving only seconds of cycle time or eliminating small amounts of waste. Individually, these changes look insignificant. Collectively, over decades, they have been central to Toyota's reputation for manufacturing consistency and reliability — an advantage built one small change at a time rather than through occasional large transformation projects. 5.2 3M - Structured Time for Incremental Innovation3M's long-standing "15% Rule" gave technical employees a share of their time to pursue self-directed experiments and process refinements, independent of whether an immediate business case existed. Many of the resulting improvements were modest; the accumulated effect was a durable pipeline of incremental gains and occasional breakthrough products. The lesson for a yield-improvement decision is similar: the value of the practice lies in what it compounds into, not in any single experiment's standalone return. 5.3 Amazon - Operational Metrics That Are Never "Finished"Amazon's fulfilment operations continuously iterate on metrics such as pick time, travel distance within a warehouse, and error rate, even after a facility is already performing well by industry standards. No single tweak to a warehouse layout looks transformative in isolation. Sustained over many facilities and years, this discipline has been a meaningful contributor to the cost and speed advantages that support the company's delivery promises. 6. ComparisonPoint that organizations should stop investing once diminishing returns appear. The core flaw in that argument is that diminishing financial returns do not necessarily mean diminishing strategic value. The proposed initiative should not be evaluated solely on ROI, payback period, or implementation cost. It should also weigh future quality capability, organizational learning, customer trust, operational resilience, and competitive differentiation. Dimension View A — ROI-Only Lens View B — Strategic Lens Decision basis Payback period, five-year NPV ROI plus capability, quality culture, and risk Time horizon Project-level, 3–5 years Organizational, 10+ years What's counted Direct, quantifiable savings Direct savings plus warranty, brand, learning effects Risk treatment Assumes today's environment persists Assumes competitors and standards will keep moving Failure mode if wrong Under-invests; erodes quality edge over time Over-invests in a low-yield project AI's role Sets the go/no-go threshold Ranks and informs; humans set the threshold Table 3 — Where an ROI-only screen and a strategic screen diverge Many of the world's highest-performing organizations maintain their lead precisely because they keep improving after competitors have decided they are "good enough." A stop-at-diminishing-returns rule effectively hands that discipline to competitors who don't apply it. 7. ConclusionAI should recommend and prioritize; it should not determine the endpoint of improvement. Continuous improvement is a strategic philosophy that builds long-term resilience, innovation capacity, and competitive advantage. Individual gains, such as raising first-pass yield from 99.8% to 99.9%, may appear marginal in isolation, but their cumulative effect in defects avoided, capability built, and risk hedged — creates operational excellence that competitors often struggle to replicate. The organizations that remain world-class are rarely those that stop improving; they are the ones that keep refining even when the next improvement looks small.

-